2016 Global State Of The Confectionery Industry:Despite currency fluctuations and regional conflicts, sweets remain resilient

Currency devaluations complicate sales projections and year-to-year comparisons while regional conflicts continue to wreak havoc on confectionery consumption. Nonetheless, wherever there’s peace and stability, consumers want a bit of the “sweet life.”

“I say, something’s afoot, candy lovers!” Global confectionery sales to be precise. A casual comparison between last year’s global confectionery sales estimates ($198.4 billion) and this year’s ($183.5 billion) suggests a dramatic 7.5 percent decline. That’s enough to shake anyone out of the doldrums and not only raise eyebrows, but blood pressure as well.

So what’s going on here? Blame it on the strong U.S. dollar, that’s what. As happened in our 2016 Global Top 100, actual revenues, when converted from local currencies against the dollar, showed a decline. Yet, several companies that registered a dollar decline on our list actually registered strong gains in their local currencies. That’s what happens when there’s a seismic shift in currencies such as the dollar gaining strength against the euro last year.

As Jack Skelly, food analyst for Euromonitor International explains, “This is due to exchange rate fluctuations with the dollar being very strong at the moment compared to the euro.” Thus, a true comparison requires comparing chocolate to chocolate, sugar to sugar, gum to gum or in this case, fixed exchange rates to fixed exchange rates.

And that’s what we done in this year’s charts. In this instance, the fixed exchange rate for Western Europe (the world’s largest and most mature regional market) in 2014 is $51.7 billion compared to $52.6 billion, a 1.7 percent gain. That’s not necessarily anything to shout home about, but it’s still a positive step.

As Skelly says, “Growth has been slow in these markets [Western Europe] for quite some time. There is a degree of saturation in both, with manufacturers struggling to get consumers to buy more confectionery, and a wide range of new snacks entering the market, which are competing for the same snacking occasions as confectionery.”

Remarkably, Eastern Europe, which encompasses the Ukraine and Russia, posted a 7.9 percent gain in 2015, growing from $16.4 billion in confectionery sales to $17.7 billion. And this was against an ugly backdrop, the Russian-Ukrainian conflict. The fighting, coupled with a severe drop in oil prices, has wounded the Russian and Ukrainian economies.

One can argue that Russia has had endured the most severe impact, since its standard of living and economic output far outstripped the Ukraine. According to the International Monetary Fund, Russia’s economy shrank 3.7 percent in 2015.

And Bloomberg reports that some 22 million Russians now live in poverty, a 50 percent increase since 2013. Moreover, while European and U.S. economic sanctions and plunging oil prices have had a serious impact on the Russian economy, some analysts believe that there are inherent structural defects related to Putin’s return to the presidency back in 2012, which preclude any quick hopes of the recession actually ending.

Nonetheless, during the years preceding 2014, the Russians reacquainted themselves with premium domestic and imported chocolates. The bans on imports have only prompted the locals to turn toward domestic producers and/or contraband.

Unfortunately, the ruble’s decline coupled with tight credit has handicapped many local confectionery manufacturers from investing in automation and/or expansion. So, 2016 will be an interesting year.

As for the Ukraine, the good news is that the economy hit rock bottom in 2015, the World Bank estimating that the nation’s GP contracted by 10 percent. The basis for the good news spin is that — foregoing any return to military conflict — the economy can’t decline anymore and is expected to grow, albeit by 1 percent.

However, when it comes to regional growth, Latin America and the Middle East/Africa outpaced all, posting 22 and 12 percent gains, respectively.

Having experienced economic growth for the past five years, which averaged 3.6 percent annually, Latin America found itself in the beginning of a recession in 2015, growth contracting by 0.1 percent. Venezuela and Brazil were the countries hardest hit and both are continuing to face a broad range of economic and political crises. And it’s still unclear whether the looming summer Olympics will be a boon or boondoggle for Brazil.

It’s certain, however, that the emergence of a middle class, albeit different in nature amongst each specific country, coupled with a large youth population, has created a strong base for confectionery sales. The beginning of a regional recession, however, will undoubtedly have a dampening effect this year on confectionery sales.

Then, there’s the Asia Pacific market, which, despite some hiccups — mostly from China — continues to rise brightly.

Last year, the headlines raged about the weakening Chinese economy and the subsequent impact on confectionery consumption. But as Skelly points out, even though China is slowing down, the demographics are not. There’s still a huge wave of new people moving into the middle class here as well as in other markets. Even a minor increase in per capita spending on confectionery in such a hugely populated market causes ripples. Think tsunami.

In addition, manufacturers are becoming savvier in their efforts to appeal to these new consumers, he points out. This includes offering much cheaper, smaller products than in the West and reaching new cities and store-types where such confectionery has previously been unavailable.

In addition, Japan has seen quite positive gains in recent years — and unlike similarly developed economies — chocolate’s potential for growth remains rather untapped and is only now being exposed.

Travelling east and south, one reaches the Middle East and Africa. Despite the regional conflicts there, beginning with Syria, extending to Iraq, and continuing into Libya, Nigeria, Chad…well the list goes on, the region continues to evolve into a confectionery stronghold.

Where there are pockets of stability, there’s an appetite for sweets. Skelly notes that the United Arab Emirates and Saudi Arabia are leading the way in confectionery consumption, bolstered by a wealthy citizenry as well as Western immigrants working in those regions.

“Manufacturers have been highly proactive in increasing their capacity in the Middle East, particularly, with Mars, Nestlé and Ferrero all building new manufacturing sites in the region,” he says.

With regards to trends closer to home, that is the U.S. market, premium chocolate and flavorful candies is where it’s at. And there are no worries about dealing with currency conversions here and the strong dollar.

There are however, concerns about sluggish growth. National Confection Association projections for 2015 show an overall increase of 3.2 percent, primarily fueled by dollar gains (read price hikes) and not unit sales.

Granted, the future looks more promising, with estimates for 2020 pegged at $38.1 billion, an annual average gain of 1.8 percent over the five years.

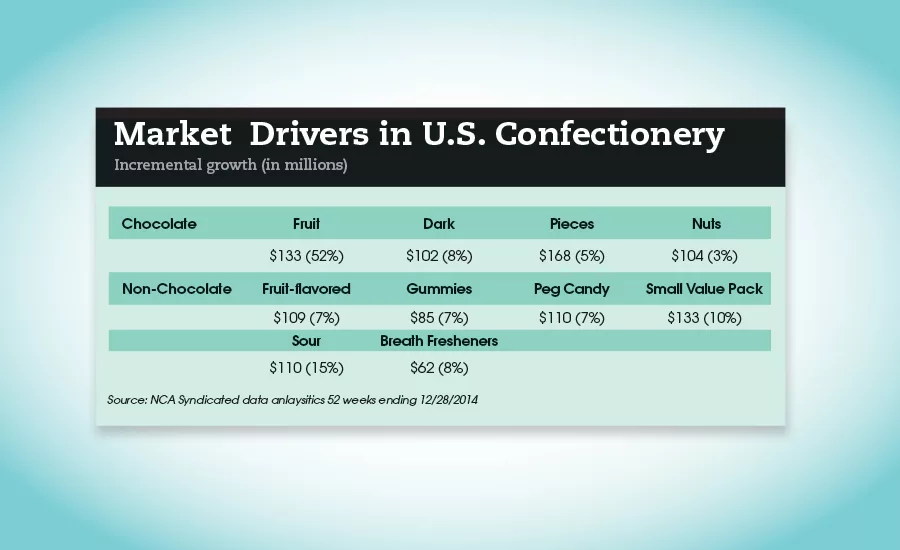

But as is always the case, there are categories outperforming the industry norm. In chocolate, the big winners, according to the NCA, were premium, seasonal and value packs. Premium chocolates grew at a rate of 15.6 percent, generating an additional $160 million in revenue. Value packs cranked out another $224 million in sales, while seasonal saw its share gain $160 million.

Chocolates that contained fruit or nuts, were shareable or were dark proved to be the drivers last year.

In addition, premium, as the name connotes, cost more, with the cost per pound averaging $11 or more during the past 24 months. And the numbers substantiate America’s appetite for better chocolate, with the premium category seeing a $15.6 percent jump in dollars, a 7.6 gain in units and an 8.3 percent uptick in volume.

On the non-chocolate side, which actually outpaced chocolate in annual gains — 3.7 percent versus 3.2 — sugar confections continued to shine. Chewy candies led the charge with $213 million in additional sales, followed by mints, which delivered $31 million in new revenue. The $245 million in new dollars sparked a 3.7 percent jump for the combined categories.

Other segments that caught consumers’ interests were fruit-flavored confections, gummies, peg candies, value packs, sours and breath mints, all registering between 7 to 10 percent gains and $609 million in additional sales.

And there was good news for gum, a category that’s seen better days in recent years. Sugarless gum, which constitutes the biggest segment of this category, saw its sales rise 1.1 percent to $2.7 billion, while gum/breath fresheners aced up 8.1 percent to $825 million. Even regular gum saw a slight bump of 0.7 percent to $528 million.

So what are the top three drivers today in the U.S. market? According to the NCA, they are the following: frequent new product launches, premium and shareables. Moreover, shareables are expected to post a 10 percent CAGR during the next five years.

The association also cites value packs, chewy candies, seasonal executions, dark chocolate, healthier inclusions and fun/daring flavor combinations as trends that will drive growth.

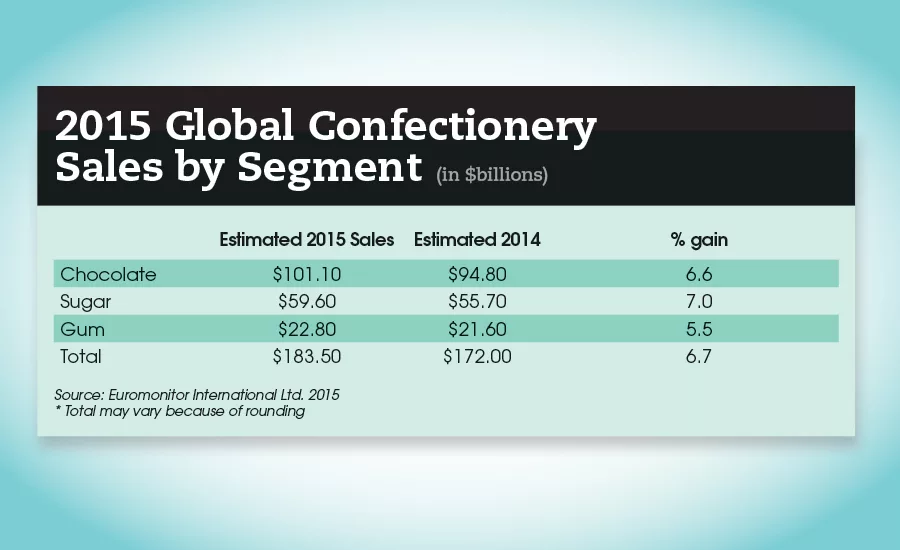

And what about a space station view of the three main segments — chocolate, sugar and gum — for global confections? Closer examination doesn’t reveal any major surprises.

Chocolate jumped from $94.8 billion in 2014 to $101.1 billion in 2015 — a 6.6 percent leap. Sugar confections enjoyed a slightly lower upshot, climbing from $55.7 billion to $59.6 billion — a 3.9 percent gain. And gum, the category that’s been hurting the most lately, displayed the smallest increase, albeit an increase nonetheless, from $21.6 billion in 2014 to $22.8 billion — a 1.2 percent step forward.

For chocolate, the big question seems to be what actually constitutes premium?

As Mintel’s Chocolate Confectionery Annual Review 2016 states, “There is no established definition for ‘premium chocolate,’ but there are some parameters that define the subcategory, based on price, perception and positioning. As premium becomes more of an everyday purchase, however, these parameters may be shifting and a discussion of premium chocolate has to be restated given the extent to which consumers have become educated about the category.”

Mintel also emphasizes what Nestlé spokesman Alessadro Rigiano said in a recent interview regarding the decision to take the company’s premium Cailler brand to a wider market, namely, that what is “the premium of today is going to be the mainstream of tomorrow.”

That statement crystallizes the progress that premium chocolate has made over the past decade. But it also raises the question of whether opportunities will continue to exist at the highest tier of premium confectionery.

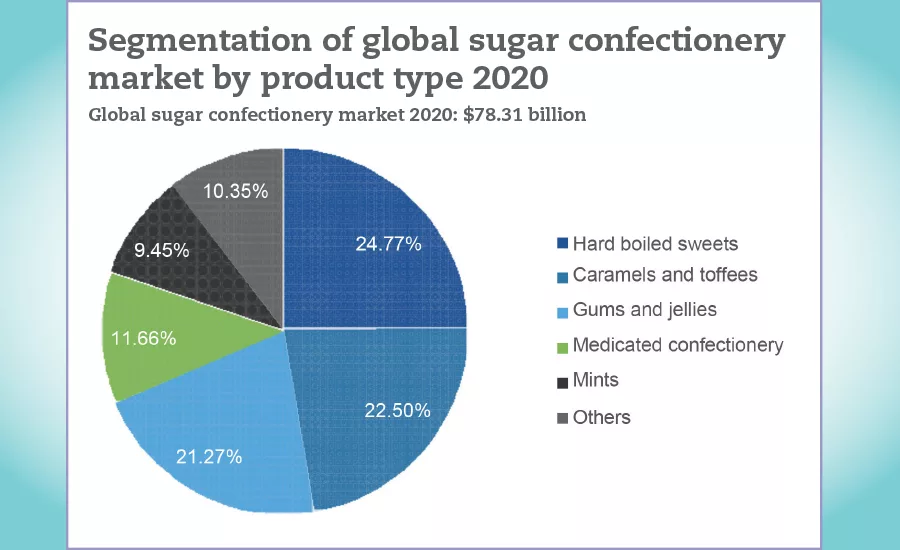

And while chocolate easily wins on glamor points and sheer obsession, the global sugar confectionery market isn’t going away. Bolstered by variety, affordability, portability, availability and innovation, sugar sweets are doing just fine, mind you.

In 2015, the Americas dominated the market, followed by Europe and Asia Pacific. However, the Asia Pacific region is projected to experience the highest growth during the forecast period.

“The demand for sugar confectionery products is increasing due to the rise in disposable incomes, urbanization, and hectic lifestyles there,” cites a recent Technavio report. The growing retail market, increasing population, and increasing trend of gifting confectionery items will also contribute to demand, the authors say. As expected, China and Japan are the major contributors in the sugar confectionery market within the Asia Pacific region.

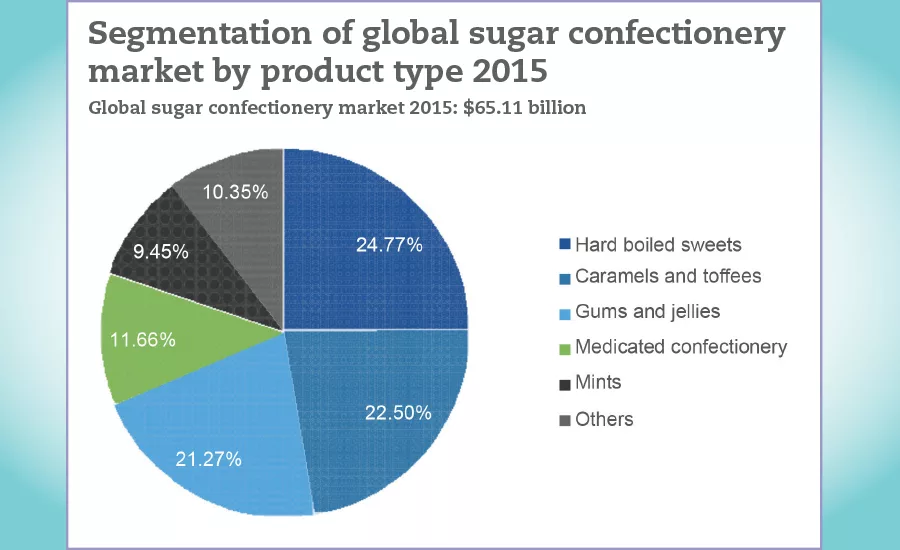

According to Technavio, the global sugar confectionery market in 2015 was estimated at $65.11 billion, a 3.56 percentage gain from the previous year. By 2020, the market should reach $78.31 billion, growing solidly at about 4 percent annually.

There are, however, some concerns as consumers seek to lose weight, monitor their health and most likely reduce sugar consumption. Here lies the opportunity for sugar-free and sugar-reduced confections, Technavio’s authors point out.

This, of course, opens the door for innovative manufacturers who are experimenting with new ingredients and sweeteners to meet the demands of a constantly evolving consumer, and a new generation of candy lovers.

As the report points out, “Manufacturers are investing in advertising to build brand identities, even though there are inherent differences in this type of product in terms of taste and ingredients. Haribo, through its advertisements, presents itself as a family brand suitable for everyone with the famous slogan, ‘Kids and grown-ups love it so.’”

As for gum, Technavio foresees a rebound for the sector. In its Global Chewing Gum Market 2015-2019, the research agency foresees a sizeable uptick, from $24.72 billion in 2014 to $32.63 billion in 2019, about 5.3 percent annual gain.

Some of the report’s key highlights:

- Using sugar-free chewing gum can reduce tooth decay — a unique selling proposition of such products.

- The preference for mints over chewing gum is likely to affect the demand for gum during the coming years. Consumers often switch to mints from gum to avoid the hassle of disposing chewing gum.

- Impulse purchasing behavior among consumers remains a key driver

- The sugar-free segment is expected to be the fastest-growing gum segment.

In addition, the report says that “Gum manufacturers today are gradually shifting away from merely focusing on taste toward producing gum with value-added benefits. This has led to the introduction of functional gum, which is gaining momentum in the global market,” the authors explain. Nicotine gum, “slimming” gum and energy gum are also expected to be key niche areas in this segment.

While most indicators point to continued solid gains in the industry, the most ominous challenge may stem from our changing lifestyles. Snacking continues to play a larger role across mature as well as emerging markets. As a result, by its very nature, it offers consumers many more choices and options.

“I think there may be a shift in the West away from impulse purchases, which are frequent and low-cost to the consumer — which I would consider snacking — to planned purchases which are less frequent but the consumer ends up spending more on chocolate when they do,” says Skelly. “This, in part, would explain why volume sales have disappointed over the last decade whilst value sales have increased. Consumers can now buy ‘highbrow,’ high quality chocolate products in their local supermarket, and so confectionery becomes a more sophisticated product than a simple snack. Given the increased presence of new rivals (such as meat snacks, energy bars such as Clif and Kind), I think this is probably a move made out of necessity by many confectionery manufacturers.

“Elsewhere, in Asia and the Middle East, I think confectionery needs to remain a snacking product in order to remain affordable to as many consumers as possible and so lay the ground work for confectionery to be a widely accessible product,” he adds.

The result? A broader product range for multinationals, niche opportunities for entrepreneurs, more blurring of the lines regarding traditional savory and sweet snacks for consumers. This is, indeed, a brave new world that candy makers and confectioners face.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!