2018 State of the Industry: Opportunities abound in confectionery market driven by snacking, treating

Global confectionery markets continue to grow.

The ubiquitous growth of global snacking, coupled with an onslaught of changes affecting consumers and customers alike, has created opportunities within a chaotic marketplace.

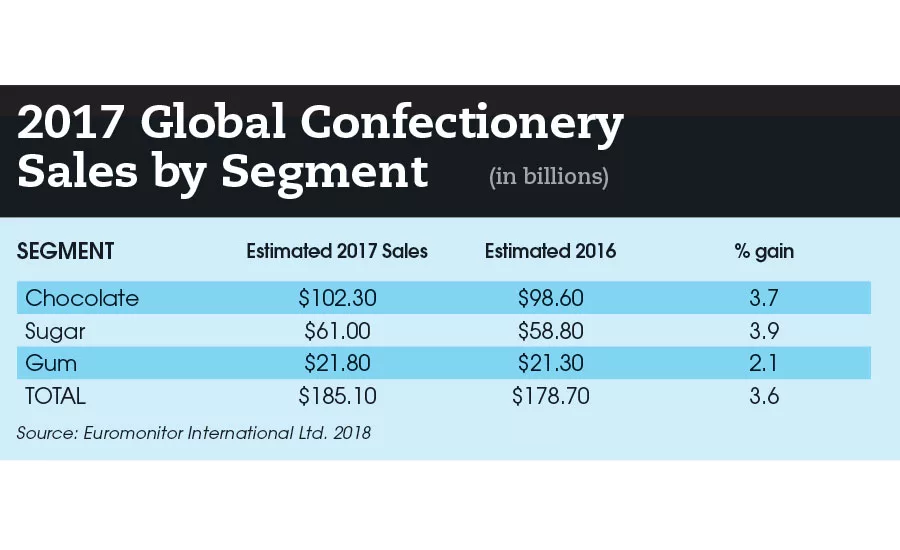

2017 Global Confectionery Sales by Segment Source: Euromonitor International Ltd. 2018 (in billions)

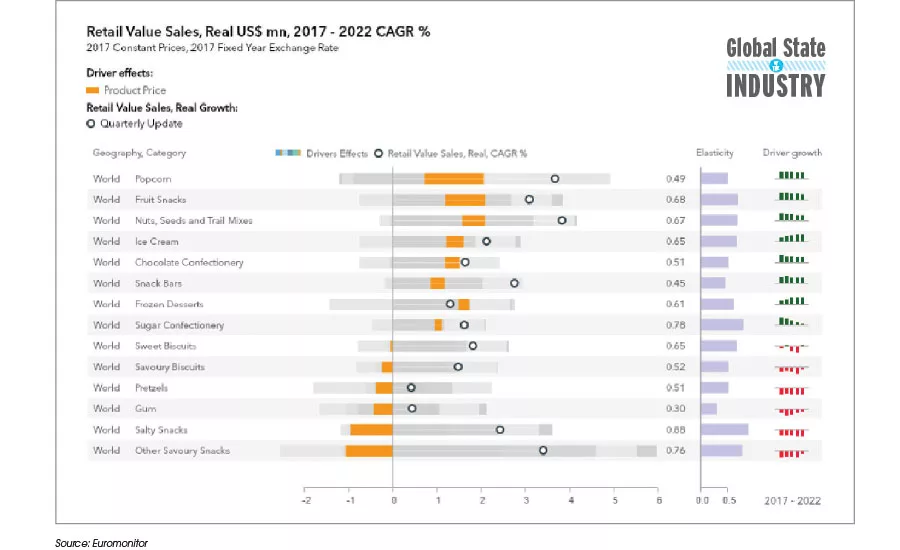

Retail Value Sales, Real US$mn, 2017-2022 CAGR%

2017 Constant Prices, 2017 Fixed Year Exchange Rate

The ubiquitous growth of global snacking, coupled with an onslaught of changes affecting consumers and customers alike, has created opportunities within a chaotic marketplace.

People buyin’ this, people buyin’ that

Why, ‘cause no one gives ‘em slack.

Ads here, ads there, but no one can hide

natural and organic, no gmos – not fried

People buyin’ this, people buyin that

Why, ‘cause no one gives ‘em slack.

Ads here, ads there, but no one can hide

Buy from me and I’ll set you free

from gluten, dairy, nuts; you’ll see

Consumers calibrated, old, young, tanks ‘n tweeds

Looking to satisfy everyone’s sweet, savory needs

Brands and better-for-you, artisans ‘n animations

Coming up with incredible, insatiable creations

Sugar’s the demon, some proselytize

but sweets can’t be all bad folks hypothesize

It’s a Ball Of Candy-fusion; that’s what the world market is today

With apologies to songwriters Norman Whitfield and Barrett Strong, who penned “Ball of Confusion” for the Temptations in 1970, I’d say both the original and the “candied” version hold relevancy in 2018.

I’ll let our readers review the original lyrics as well as the fantastic vocals by the Temptations and instrumentation by the Funk Brothers privately. But what some may call a sad attempt at “candifying” the original verse does bring out the incredible dynamics in play within the confectionery industry.

Those of us who have lived through the ‘60s and early ’70s recall the upheavals, protests, riots, polarization and eventual changes that shook the United States, and I’d say the Western World.

Still, there was the music, art and literature. Inspired by chaos — at times cruelty — as well as the need for escapism, creativity flourished. So how can one compare such history to the confectionery industry?

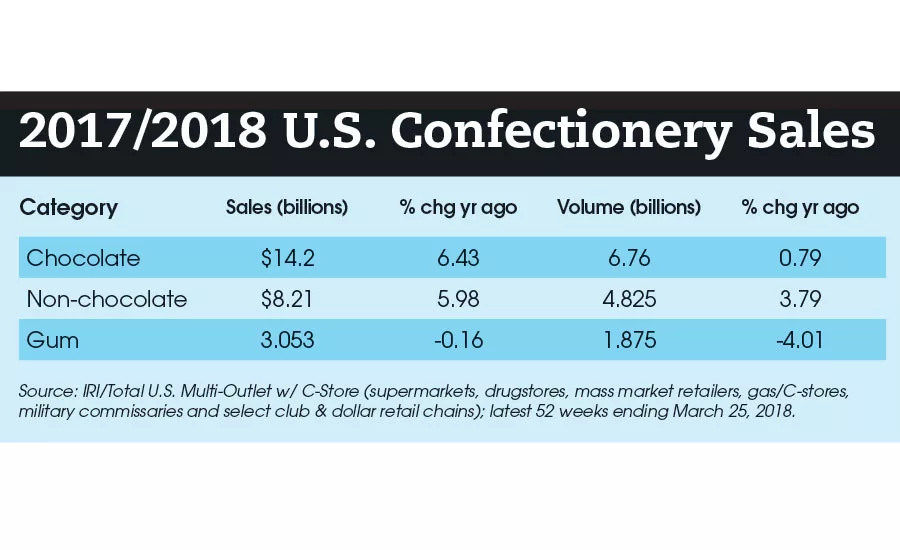

Before I get accused of having consumed too many edibles, hear me out. In case you haven’t noticed, there’s a snacking revolution going on. According to IRI, total snack sales in the United States – year ending April 22, 2018 – rose 3.4 percent to $42.5 billion. Candy sales lagged a bit, reaching $25.3 billion, a 1.4 percent increase only.

But this phenomenon isn’t limited to the world’s largest confectionery market. Snacking has become ubiquitous globally, and that represents a major shift in the ways companies are approaching new product development.

Consider how two major corporate players, Mars and Hershey, view this landscape. Earlier this year, Todd Tillemans, president – U.S., The Hershey Co., signaled where his company was heading by calling 2018, “The Year of the Snacking Powerhouse.”

“Ask anyone on the street what Hershey is, and they’ll tell you we’re a chocolate company,” he wrote. “And, in part, that’s true — we have a long, successful history in sweets and refreshments, with iconic brands that generations of consumers have fallen in love with.

“But it is also true that we have a substantial position in snacking, and we’re poised to achieve even more. For example, we recently welcomed into the fold Amplify Snacking Brands, with its stable of snacks like Skinny Pop popcorn, Paqui chips and Oatmega cookies. Amplify is our biggest acquisition ever, with brands that appeal to consumers’ growing preference for better-for-you snacks. These iconic brands are beloved by consumers and retailers alike. We are confident that the strength of our newly acquired brands, coupled with Hershey’s growing product portfolio outside of core confection, will enable us to capture more consumer snacking occasions.”

As Tillemans concluded, “Snacking leadership? We’re already there. We’re ready to take it to the next level, and we have the people, the insights, the confidence and the resolve to lead the way.”

That commentary leaves little doubt as to where Hershey’s headed.

But that’s not the direction Mars Wrigley Confectionery is going. A recently published whitepaper — “The Mars Wrigley Confectionery Treat Report: U.S. Consumer Insights on Treats and Treating” — underscored its positioning.

“As the world’s largest manufacturer of chocolate, candy, gum and mints, Mars Wrigley Confectionery is an expert on treats and the role they play in our lives,” the report emphasized.

Updating an earlier survey on how consumers view treats, the company released findings gleaned last year from such research.

“Findings show that across all age groups, Americans see treats as a special indulgence. Nearly all (98%) of respondents believe that a healthy lifestyle includes an occasional sweet treat. This is in line with what Mars Wrigley Confectionery believes – that chocolate and candy is a treat, not a snack or meal replacement. That’s why we’ve partnered with the Partnership for a Healthier America to purposefully position chocolate and candy as a treat, and have committed to give consumers the information, options and support they need as they choose how to enjoy their favorite treats.”

So, is snacks or treats? Or can one take a two-pronged approach? Another global competitor, Mondelez International, is well positioned to do so with its stable of sweet and snacking brands. Nonetheless, that doesn’t automatically guarantee success today or tomorrow.

For example, an analysis of Mondelez’s performance by Seeking Alpha, a stock market insights and financial analysis group, summed the situation like this: “The dynamics of the global packaged food industry are evolving, health-oriented organic and gluten-free products having low calories will drive growth in future sales. The challenge, however, is that the chocolate confectionery and sweet biscuits categories will underperform savory snacks, snack bars, and nuts & seeds and trail mixes over the next five years, which is an immense downside risk for Mondelez.”

A quick review of various snacking categories shown in the Euromonitor chart, including chocolate, sugar and gum, underscores that kind of thinking. While compound annual growth rates (CAGR) for the five-year period (2017-2022) of 0.51 and 0.78, respectively, bode well, the salty and savory snack numbers, 0.88 and 0.76 fare better.

But let’s step back and see what happened in 2017 before we can extrapolate what lies ahead. At first glance, despite all the turmoil, confectionery seems to be a rather stable marketplace. Euromonitor estimates that the chocolate, sugar and gum categories all grew, delivering a 3.6 percent gain in 2017 for the global confectionery industry. Total sales grew from $178.7 billion to $185.1 billion.

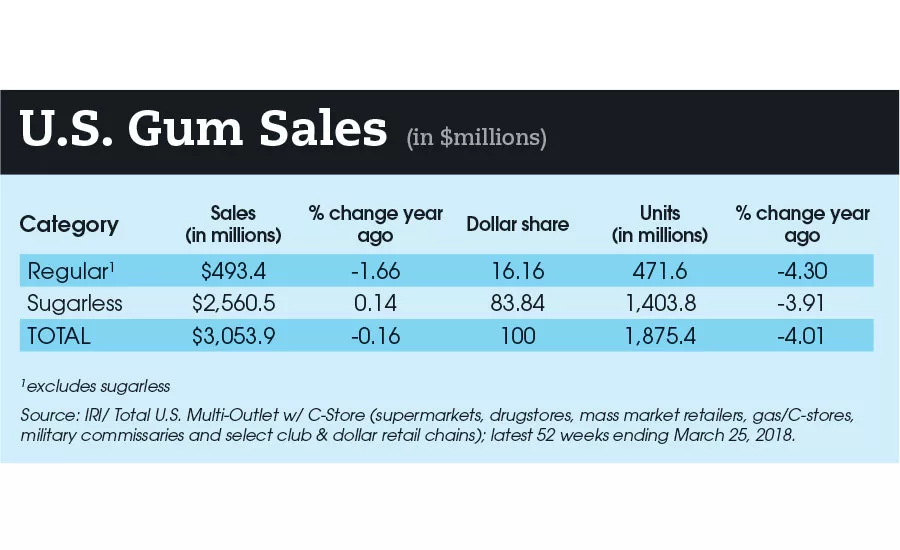

Unlike last year, however, the growth category proved to be in sugar, with a 3.9 percent jump from last year. Chocolate, while still generating the largest revenues, posted a slightly lesser gain of 3.7 percent. The gum category, however, continues to struggle, generating just a 2.1 percent increase from last year.

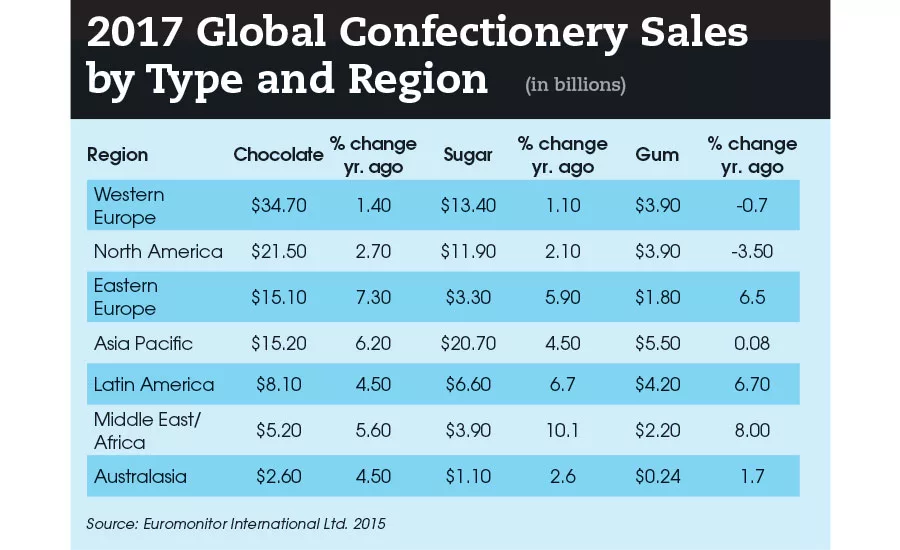

Global regional growth numbers reinforce the dynamism in emerging markets, despite dealing with conflict, oppressive and/or unstable governments and fragile or damaged infrastructures. The mega-but-mature markets, such as Western Europe and North America, reflect those changing consumer attitudes and lifestyles mentioned earlier. The Middle East/Africa, Latin America and Asia Pacific regions, blessed with rising incomes among working and middle classes in certain countries, as well as larger youth demographics, are ripe for increased confectionery consumption and experimentation.

Add to that a penchant for sweets in some nations, and the opportunities loom even larger.

A GlobalData report, for example, cites the release of Pulse hard-boiled sweets by DS Group in India as an example of tapping into local tastes and traditions. Thus, by incorporating flavors “such as raw mango, guava, pineapple and orange, with a tangy core,” the hard candies became “an instant hit as consuming fruits such as raw mango and guava with a spicy accompaniment is a popular practice among Indians.”

With two years of its launch, Pulse candies hit $46 million in sales, inducing competitors to follow suit, of course.

The ongoing shift toward better-for-you confections doesn’t necessarily bode bad news for iconic brands. First, as has been cited ad infinitum by trend watchers: for every trend, there’s a counter trend.

Moreover, consumers are complex purchasing agents. They refuse to be thrust into any convenient marketing slot, surprising and vexing marketing analysts and researchers. A Snickers patron, for example, may opt for a caffeinated toffee as a matter of convenience and need. Or they could choose an all-natural, fruit juice-filled gummy to stimulate the senses during a boring webinar.

Hence, large and small manufacturers are coming to grips with taking advantage of this “health halo” affecting everything we consume, despite ignoring some of the very tenets of what a healthy lifestyle should be.

Earlier this year Nestlé launched Milkybar Wowsomes in the UK and Ireland, a reduced sugar version of its Milkybar brand. The company claimed this was the first chocolate bar in the world to use “uniquely structured particles of sugar to deliver 30 percent less sugar.”

According to Tom Vierhile, Innovation Insights Director at GlobalData, this was a game changer.

‘‘Nestlé’s breakthrough technology for Milkybar Wowsomes could change the sugar reduction game in the confectionery industry as the product does not rely on challenging controversial alternatives to conventional sugar (like stevia, aspartame, or sucralose) to reduce sugar content,” he said. “Our 2017 Q4 consumer survey found that 52 percent of UK consumers say that ‘low in sugar’ means ‘healthy’ to them, a significantly higher percentage than the 44 percent of consumers globally who express this sentiment. This suggests that Nestlé may find a curious and willing audience in the UK for Milkybar Wowsomes and its breakthrough sugar technology.”

What makes the sugar-reduction process in Milkybar Wowsomes unique is that the candy technologists were inspired by candy floss (cotton candy) in finding a way to reduce sugar content. The structure of the sugar used in Milkybar Wowsomes has been changed into porous particles said to dissolve more quickly in the mouth than conventional sugar.

But according to Nestlé, their new restructured sugar formula delivers the same perceived level of sweetness as a product sweetened with conventional sugar, but with less sugar, of course.

It’s an important marketing claim, Vierhiel asserted.

‘‘Consumers are much more focused on the sugar content of their food and drink products these days,” he said. “According to our 2017 Q4 consumer survey, 81 percent of UK consumers say they are paying attention to sugar or sweeteners in food and drink products. While that is below the 84 percent of Europeans and 87 percent of consumers globally that say the same thing, we feel that this gap may narrow thanks to interventions like the UK sugar tax, which injects economic pain into making product choices that may be health-challenged.

“The confectionery industry was probably lucky to avoid the so-called ‘sugar tax’ in the UK which is aimed at sugary drinks, but that luck may not last forever,” Vierhiel added. “It may only be a matter of time before confectionery is subject to a ‘sugar tax’ of its own. Ingredient innovations like restructured sugar will make it a lot easier for some FMCG brands to achieve sugar reduction goals while curbing the call for the consumer to ‘sacrifice’ by consuming less product.”

As always, it’s important to remember that not all consumers “sacrifice,” some merely switch. In a recent State of the Market presentation that debuted at the National Confectioners Association (NCA)’s Sweets & Snacks Expo, IRI Executive Vice Presidents Larry Levin and Sally Lyons Wyatt pointed out that 13,000 new brands were launched in 2017.

Of those, only 200 made IRI’s New Product Pacesetter (NPP) status. And in that context, only four brands broke through the $100-million mark. Despite those rather dismal numbers, it’s innovation that’s driving the categories.

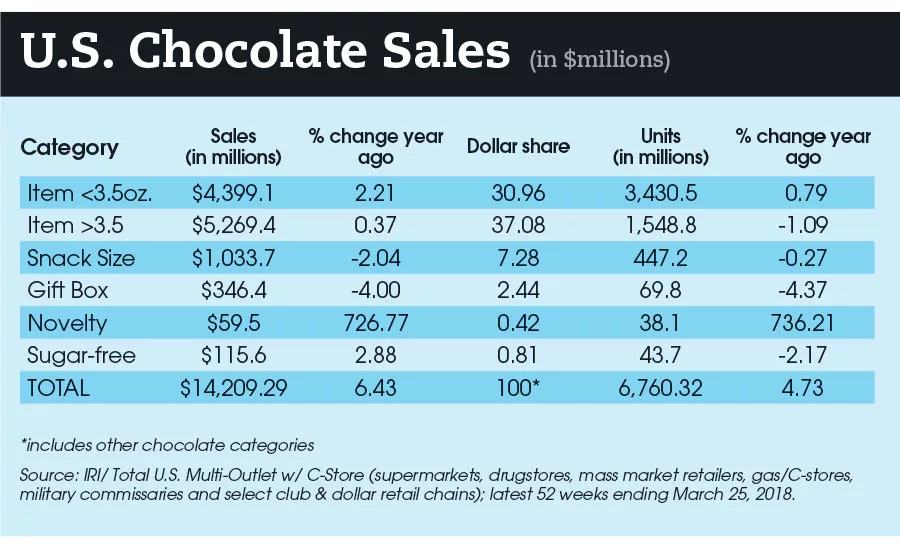

Within the chocolate category, IRI attributes $1.6 billion in sales of the $14-billion segment directly to “chocolate innovation,” i.e., new product launches. Within that $1.6-billion bucket, $1.1 billion is attributed to everyday innovation, the remaining $570 million to holiday items.

In taking a closer look at the IRI NPP list in confections and snacks, three were health bars: No. 5, Special K Nourish Breakfast Bars, posting $25.5 million; No. 8, Pressed by Kind, racking up $15.2 million in its debut; and No. 9, Oatmega Nutritional Bars, hitting $14.5 million.

Good Thins, a thin cracker produced by Nabisco containing no corn syrup, partially hydrogenated oils, artificial colors and gluten, topped IRI’s NPP’s list, approaching the $90-million mark ($87) in its debut. Only two items — Hershey’s Cookie Layer Crunch (No. 2 at $47.7 million) and Milka Oreo Chocolate Candy (No. 3 at $43.9 million) — represented what some may call traditional chocolate confections, albeit as hybrids. And Black Forest Organic Candy Drops slipped into the Top 10 with $14.2 million in sales.

Salty snack items such as Doritos Mix (No. 4 at $28.6 million), Pringles Loud (No. 6 at $18.3 million) and Sunchips Veggie Harvest (No. 7 at $17.4 million) filled out the remaining NPP slots in the Top 10.

It does not come as a surprise that after revealing its Top NPPs, IRI declared non-GMO, gluten-free and organic claims as key drivers in confectionery sales. Those boasting non-GMO Project Verified claims shot up 42.7 percent within chocolate (85.5 million) and 59 percent in non-chocolate.

Organic claims in chocolate have increased 15.4 percent, representing $68.2 million in new product sales while non-chocolate claims have soared 58.6 percent, comprising $33.5 million in sales. Gluten-free claims also continue to grow, with new chocolate products seeing an 18.8 percent increase ($112.1 million) and non-chocolate a 13.2 jump ($238.4 million).

Given these ongoing patterns in better-for-you claims, one also sees a surge in vegan confectionery product launches. Mintel data reveals that between 2013 and 2017, vegan confectionery product launches more than doubled, growing by 140 percent.

“There has been a growth in non-dairy milk chocolate, while in sugar confectionery there is growing interest in vegetable-based gelatin,” says Marcia Mogelonsky, Mintel’s food and drink director of insight. “Growing awareness of the source of certain ingredients, such as gelatin in confectionery products, is making consumers more conscious in their purchase decisions.”

That, of course, doesn’t mean confectionery manufacturers producing traditional sweets face extinction.

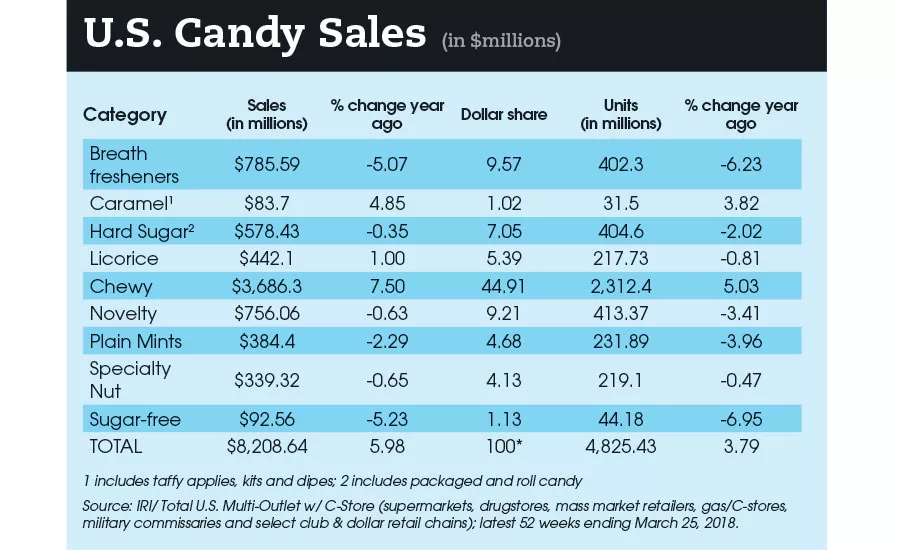

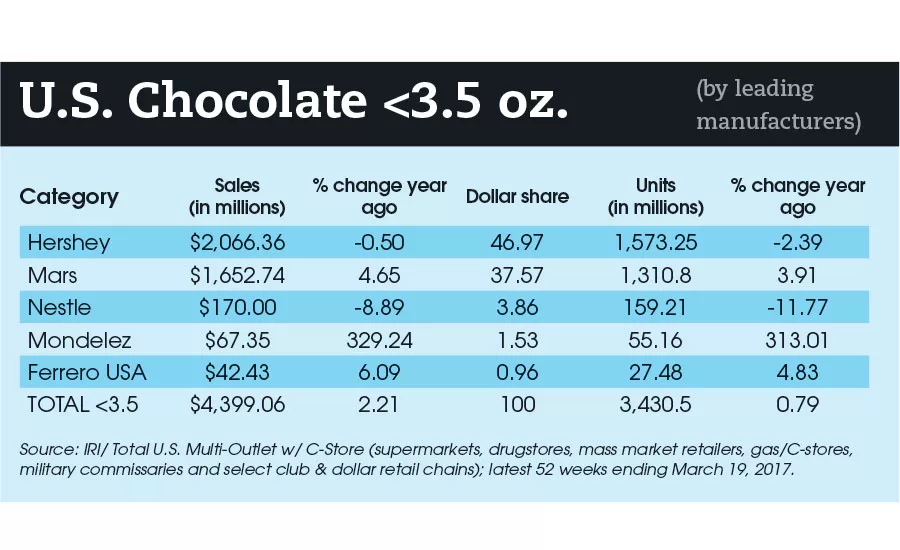

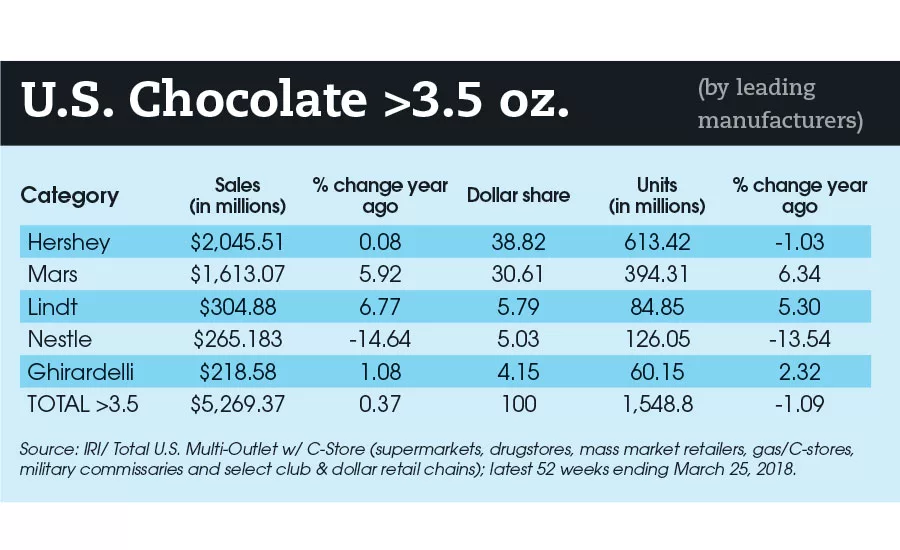

A review of the various categories detailed in the accompanying chart belies that fear. But as John Downs, president of the NCA pointed out at a recent speech given at Chocovision in Davos, Switzerland, there are changes in the works.

“No matter how the industry changes and shifts in the years to come, we know our category will continue to be relevant and grow,” Downs said. “How can we be sure? Because there is no end in sight to the emotional and social connections that consumers have with our products.

“In fact 90 percent of Americans have said that a world without chocolate and candy is no world at all. But, that does not shield us from the same disruptions that face other industries. We need to be radically open-minded about these challenges, while still being mindful of the opportunities they present.”

In that Temptations song, there’s a verse subtly warning about ignoring changes: “And the band played on.” Despite the confusing trends and counter-trends affecting the confectionery industry, it remains critically important to keep one’s eye on the ball, especially as it morphs before our eyes.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!