Cold storage strategies

Cold chain is an important factor in the snack and bakery industry. If cold storage capacity is at its fullest, that affects the safety of products, and thus consumers.

Macro trends affecting the cold storage industry include consolidation and capacity, says Corey Rosenbusch, president and CEO, GEA, Arlington, VA. “The cold chain industry has garnered attention from institutional investors and private equity firms because of the industry’s strong financial performance over the last several years, due to cold chain industry characteristics—we’re recession resilient, have a growing population to feed, and see customer diversification over many product types.”

Much of the growth in cold storage warehouses has been organic, notes Rosenbusch. However, acquisitions are increasingly used to fuel growth. “Between 2009 and 2019, there were 68 acquisitions—11 in 2019 alone. Currently, over 20 private equity firms have a position in a cold storage facility.”

It can be challenging, in some markets, for food companies to find cold storage space, as demand exceeds supply, says Rosenbusch. “This creates favorable market conditions for the cold storage industry but makes it difficult for smaller food companies with lower volumes to find a cold storage partner. Cold storage capacity in the U.S. is tight and has been for the past few years. We have seen occupancy of cold storage facilities average 86 percent. Many facilities consider 82–84 percent full, as they need space to operate and manage distribution.”

Cold storage capacity is impacted by inventories for all perishable commodities, says Rosenbusch. There are a number of factors that influence capacity, including:

- Increases in SKUs and inventories to meet retailer demands

- Increases/changes in production

- Trade issues

Also, there is currently a labor shortage in the cold chain industry, says Rosenbusch. “The labor situation in the cold chain industry differs by segment. For example, cold storage warehouse turnover is down while there is a shortage of refrigerated trucks on the distribution side,” he says.

The labor shortage is still a challenge for the cold chain industry, but strategic efforts to retain employees to lessen the effects of the shortage appear to be working, according to results of the 2019 IARW North American Warehouse Employee Turnover Survey that measures turnover rates from January 2018 through December 2018, notes Rosenbusch.

“In our 2018 survey, respondents reported an employee turnover rate of 40.2 percent, but our 2019 survey shows a significant decrease—32.8 percent—which is 7.4 percent lower than the previous year,” says Catharine Perry, vice president of member programs and services, Global Cold Chain Alliance, Arlington, VA.

Trucking is the lifeblood of the cold chain. Yet, there is a current overall shortage of 51,000 drivers, estimated to grow as high as 170,000 by 2026, notes Matt Luckas, vice president, supply chain service, Hanson Logistics, St. Joseph, MI.

The problem is equally bad in Europe, where one-fifth of driver positions reportedly are unfilled, and the shortage in the United Kingdom is estimated to be growing at 50 drivers a day, says Rosenbusch.

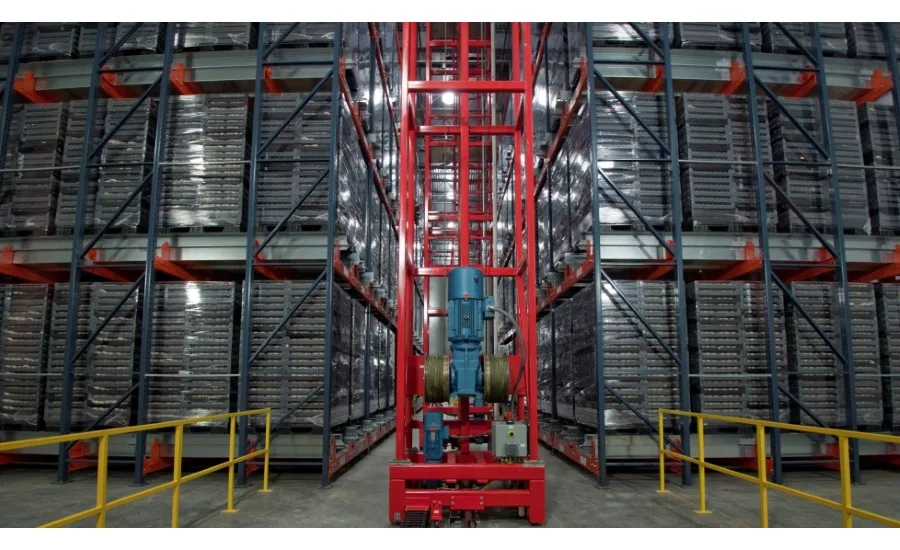

For temperature-controlled warehouses, the largest cost is labor and the U.S. unemployment rates are very low, notes Rosenbusch. “Therefore, we’ve reached a tipping point where automation has become a very viable way to augment labor. We see demand for cold chain technology that efficiently and effectively addresses these costs. For example, many cold storage companies are investing in automation that enables more efficient labor usage. We also see new refrigeration technologies that help reduce energy usage and contribute to customers’ sustainability goals.”

Sustainable technology issues in the cold chain industry include solar, fuel cells, battery storage, battery technology like lithium ion, lighting, Variable Frequency Drives (VFDS), and ECM motors, says Rosenbusch.

In addition, meeting consumers’ expectations for quick and reliable delivery of fresh foods has created a need for regional public warehouses (3PLs) that can provide just-in-time service for grocery stores as well as their consumers, Rosenbusch comments.

Frozen business has been increasing over the past three years, says Neil Garrett, H&S/NEF director of quality and continuous improvement, Northeast Foods, Baltimore, MD. “Clean label is contributing to fast food restaurants transitioning to frozen,” he says. “The impact to baking is finding freezing facilities that are strategically located.”

More markets going to frozen line of operation is partially due to the lack of skilled bakers/labor, and the resulting effect is lower product quality and lack of product consistency, Garrett notes. “The industry is shifting to frozen to reduce waste and minimize downtime. Extended run times allows for greater efficiency over a sustained period and the ability to adjust the processing equipment to meet specifications set by the customers.”

In addition to the labor challenge, it also provides convenience for suppliers that do not have sufficient space and/or time to bake from scratch the ability to offer a wide array of products for their customers, Garrett remarks. “The draw of frozen for foodservice is it allows an operator to provide consistent, fresh, high quality product at any given moment to meet consumer demand.”

There has been an increase in freezing due to the fast food industry pushing for a cleaner product label, he says.

“NEF added two freezers to our bakeries last year to accommodate the need for freezing. Our fast food business is 84 percent frozen, and growing,” he adds.

Consumer preferences

Consumer buying patterns do have an impact on the cold storage industry, says Rosenbusch.

“Warehouses are working closely with their customers as trends like e-commerce and grocery deliver emerge. These trends provide opportunities for warehouses to provide additional value-added services as they strive to be a complete supply chain solution for their customers,” he explains.

Evolving buying patterns can also impact inventory at facilities, as the numbers of SKUs has continued to increase in recent years, and some companies are choosing to store larger inventories to enable a more nimble response to retailer demands, Rosenbusch notes. “While e-commerce and other delivery channels such as click and collect are growing, they still represent a small percentage of total retail; and thus, much of cold storage operation remain unchanged.”

Increased consumer demand for produce is impacting cold storage development around the globe, Rosenbusch adds. “For example, the maturation of Asian markets, and regions where populations are seeing improved living conditions and increased purchasing power, are feeding the demand for European produce exports. The new cold storage facilities for the export of fruit and the new distribution centers for all the supermarket groups has brought growth in the cold chain sector that is far above the national economic growth of South Africa.”

In addition, international trade is an important component of many of GCCA’s warehouse members’ businesses. “As a result, trade policy is of key interest to our industry. Trade uncertainties can have a variety of impacts. In some cases, products are channeled into alternative markets. In other cases, inventories in storage may increase as tariffs or other policies are instituted, and inventory turns slow,” explains Rosenbusch.

In addition to a focus on U.S. regulatory agencies (such as the USDA and FDA), GCCA’s advocacy team focuses attention on matters that impact the import and export of perishables in the food industry. Currently, some key trade policy issues for the cold chain industry include: the U.S.–Mexico–Canada Agreement (USMCA), the US Department of Agriculture’s Public Health Information System (PHIS) Export Component, and demurrage requirements for multi-modal travel.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!