State of the Industry 2016: Meeting today’s bakery market demands

Bakery companies across the industry have built incremental growth through strategic product and line launches that meet the changing demographic demands.

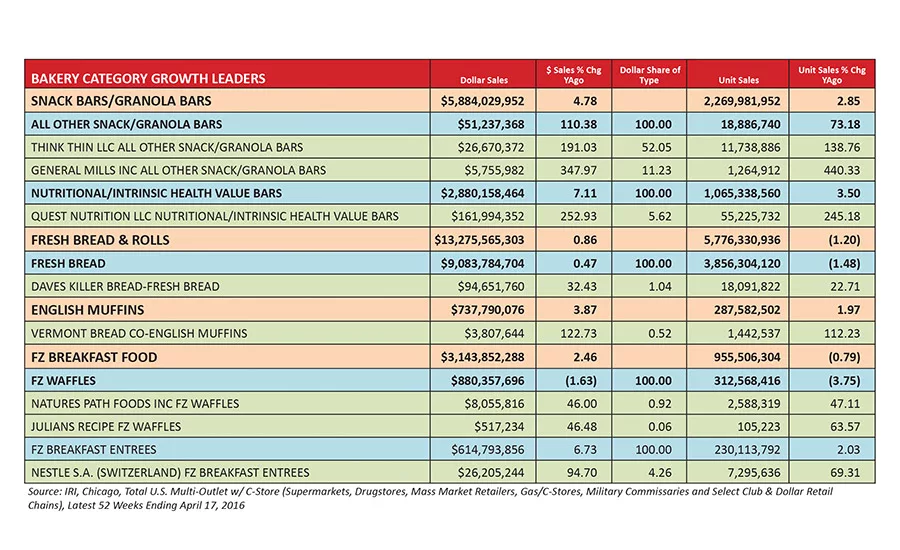

Bakery Category Growth Leaders

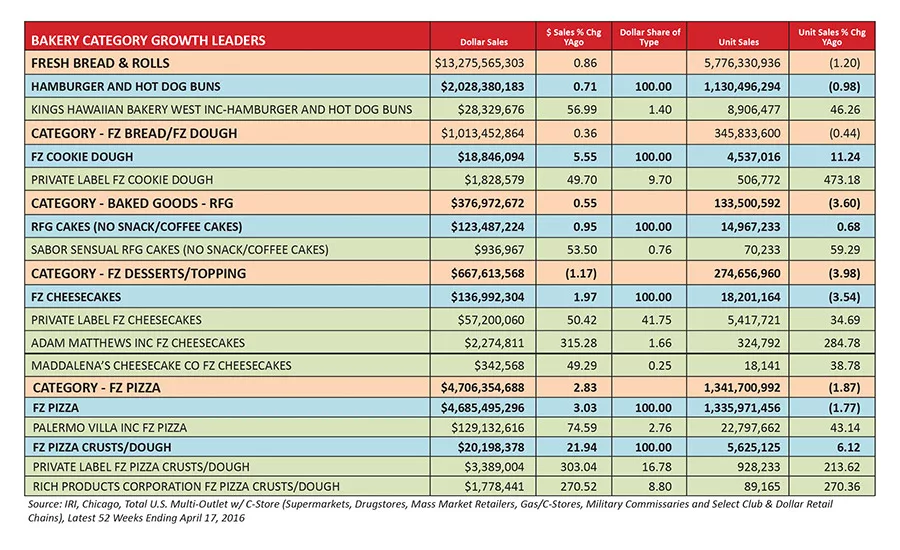

Bakery Category Growth Leaders

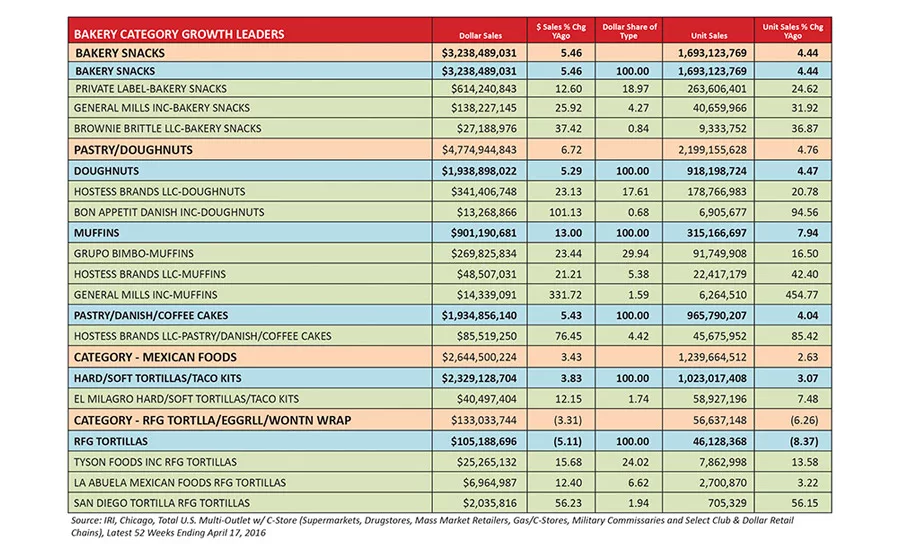

Bakery Category Growth Leaders

Tradition is the foundation that grounds much of the bakery industry’s continued success. We see this immutable fact across nearly every category, with leading companies selling billions of dollars of traditional baked goods that have long stood the test of time. These are core products beloved by millions of shoppers.

Overview | Bread | Tortillas | Sweet Goods | Snack Cakes | Pizza | Desserts | Cookies | Buns & Rolls | Bars | Breakfast Products

But innovation is the fuel of the incremental gains we see across nearly every category in bakery today. This comes via the snackification of bakery products to meet the needs of on-the-go folks from coast to coast. It comes via truly better-for-you formulations that stand up to Nutrition Facts scrutiny. And it comes from a wide range of more-nebulous better-for-you sentiments pervading the food industry today.

In the end, the goal is a sufficiently diversified product mix that appeals to the greatest percentage of U.S. consumers—which is no small feat considering the wide range of factors at play in the industry today.

Looking back

The bakery industry saw numerous companies and products take the lead in terms of overall sales growth over the 52 weeks ending April 17, 2016.

General Mills saw strong acceleration of its bars segment, up 347.97 percent in dollar sales for the year, per IRI, Chicago. The company offers several bar brands that meet a wide range of shopper demographics, including Nature Valley, which saw notable growth of 485.43 percent for its Roasted Nut Crunch line. Other bar lines in the General Mills stable include Lärabar, Fiber One, Annie’s and Cascadian Farm. Its category-banding Epic brand bars go Paleo and combine meats with seeds and fruits.

Bars is a perennially hot category, and this past year was no exception. Quest Nutrition also saw significant sales growth of its nutritionally targeted bars, up 252.93 percent in dollar sales for the year.

In fresh bread, all eyes will be on Dave’s Killer Bread over the coming year as Flowers Foods takes the better-for-you brand to a national audience. Over the past year, it far outpaced the category, up 32.43 percent in dollar sales. Expect to see that number climb over the coming year—along with other better-for-you breads that fit the increasing range of organic, all-natural, highly seeded, nutritionally dense products hitting the market.

King’s Hawaiian continues to show strength across buns and rolls. While it remains at the No. 2 spot for all other fresh rolls/bun/croissants for the past year, up 13.63 percent in dollar sales, it led all growth in the hamburger and hot dog buns segment, up 56.99 percent.

Refrigerated cakes is a minor category in bakery, and one that saw only 0.95 percent in dollar sales gain over the past year. But Sabor Sensual, a Taste It Presents brand, broke through in a big way with 53.50 percent growth in dollar sales. The brand targets the Latin American market with authentic products like Tres Leches Cake.

Adam Matthews likewise brings the stability of tradition to its frozen cheesecakes. While the company offers classic varieties, it also branches into products of unbridled indulgence like Chocolate Chocolate Chip, Chunky Brownie and Mint Chocolate Chip, among others. Adam Matthews also offers offers retailers scaled-down, affordable indulgence via packaging that combines two slices of cheesecake. Dollar sales of the company’s frozen cheesecake were up 315.28 percent for the year.

In frozen pizza, Palermo Villa found a willing market for its super premium pizza lines, such as its Screamin’ Sicilian brand, up 326.26 percent in dollar sales. Overall, the company saw dollar sales growth of 74.59 percent. Growth of the super premium segment of frozen pizza illustrates an increasing shopper desire for quality reminiscent of pizzerias in the freezer case.

Muffins saw an improvement over the past year, up 13.00 percent in dollar sales compared to the 7.13 percent growth seen in 2015. General Mills clearly found a market for its muffins, with dollar sales growth of 331.72 percent. Elsewhere in the sweet goods category, Hostess Brands had a solid year in pastry/Danish/coffee cakes, up 76.45 percent. And in doughnuts, Bon Appetit grew its dollar sales by 101.13 percent. Its miniature doughnuts come in classic flavors like Chocolate, Crumb and Powdered.

Mintel, Chicago, has noted several trends driving the bakery industry forward of late. One of these is the snackification of breakfast via portion-controlled baked goods that permit on-the-go consumption. One successful product in this area is breakfast cookies/biscuits, but other opportunities exist for snack-sized fresh bread products for breakfast sandwiches and savory breakfast breads.

Mintel also points toward hybrid baked goods—particularly those that fit within the sweet goods category—to drive sales. Products that cross elements of doughnuts and croissants (Cronuts), doughnuts and muffins (Duffins), and doughnuts and waffles (Wonuts) have been popularly cited as examples.

Private label maintains a position of strength in bakery across the store. According to the 2016 Private Label Manufacturers Association (PLMA) “Private Label Yearbook,” private label bread and baked goods accounted for $4.2 billion in supermarket sales for 2015, capturing 28.8 percent of total dollar share (PLMA collaborates with Nielsen on its sales data). This makes bread and baked goods the No. 3 segment for private label, just behind milk and cheese. When all retail outlets are combined—across U.S. supermarkets, drug chains, mass merchandisers, warehouse/club stores, dollar stores and military exchanges—dollar sales of bread and baked goods climb to $6.7 billion for 30.2 percent of dollar share. In terms of total unit sales, bread and baked goods move ahead of cheese, accounting for 2.0 billion units sold, capturing 35.0 percent of unit share.

The ongoing strength of private label bakery products makes a good case for businesses to diversify strategic plans to include private label as part of the markets served, in addition to branded retail and foodservice.

In foodservice, coffee café, bakery-café, fast-casual and fast-food/quick-service restaurant (QSR) segments—all part of the larger limited-service restaurant (LSR) category—offer significant opportunities to bakeries. According to the 2016 “Top 500 Chain Restaurant Report” from Technomic, Chicago, sales—based on menu types—grew from 2014 to 2015 across many of these areas of foodservice:

- Coffee cafés—up 9.9 percent

- Bakery-cafés—up 6.7 percent

- Pizza—up 5.9 percent

- Sandwich—up 2.7 percent

Technomic notes that some of the key takeaways and themes of 2015 across foodservice include:

- Clean eating and labeling

- Demand for “better” everything

- The power of “QSR Plus”

- All-day breakfast

- Food with a story

Technomic coined the “QSR Plus” term to describe the restaurant segment that straddles traditional QSR and fast-casual. QSR Plus restaurants generally have relatively limited menus, but higher quality than typical QSRs—and with slightly higher price points than QSR, but lower than fast-casual. Three examples of this emerging segment include Chick-fil-A, Culver’s and Potbelly Sandwich Shop. Artisan or gourmet buns can serve as differentiating points in such sandwich-centric chain restaurants.

The LSR bakery-café segment continues to see strong sales performance. According to Technomic, segment leader Panera Bread saw sales rise by 7.1 percent in 2015 to $4.8 billion. Panera accounts for a 60.6 percent share of all bakery-café sales. Another concept, Kneaders Bakery & Café, is seeing the strongest growth in the segment, with a 40.0 percent increase in sales for the year and an increase in total units by over 60 percent. Other bakery-café chains showing strong growth, per Technomic, include Boudin Sourdough Bakery & Café, Le Pain Quotidien, Alonti Catering Café and Specialty’s Café & Bakery.

Looking forward

As bakers continue to seek incremental sales gains through new product introductions, better-for-you dynamics like clean label, non-GMO, portion control and others will come into play.

An emerging area of note in bakery is the switch from conventional to cage-free eggs—an aspect of ingredient sourcing that a handful of prominent bakery companies have recently highlighted. The ARYZTA brand Otis Spunkmeyer has announced that it will incorporate cage-free eggs into its retail lines of snack cakes and sweet goods by the end of 2018, with 100 percent of products using cage-free eggs by the end of 2023. More immediately, the company’s La Brea Bakery brand will begin transitioning to use of cage-free eggs this year. Nestlé has also committed to 100 percent use of cage-free eggs by 2020.

As animal-welfare concerns like these ingrain themselves into the food industry as a whole, we can expect them to begin surfacing in leading baked goods, helping craft a point of differentiation that will resonate with shopper demographics hungry for every possible detail related to the origins and dynamics of the bakery brands they buy. These concerns will also challenge suppliers to meet newfound demand across the entire bakery industry.

Other product characteristics more clearly and directly related to better-for-you concerns will also factor into development of new products and lines. The updated design of the new Nutrition Facts panel clearly highlights calories and servings. It also will include a line for “added sugars.” These two points will likely combine to encourage bakers to work toward cutting down calorie counts through formulation strategies that reduce the total level of added sugars to create a competitive advantage within shopper demographics prone to making side-by-side product comparisons—as long as the products don’t sacrifice on overall taste and perceived indulgence.

The bakery industry today is a smart combination of tradition and innovation, and we need both to maintain upward business trajectories. But much of the category growth we see will come via the mega-trend of better-for-you in the coming years. Success will come through offering the right level of product diversity that aligns with prevailing ingredient, packaging and other trends to meet the needs of increasingly attentive and discerning U.S. shopper demographics.

Overview | Bread | Tortillas | Sweet Goods | Snack Cakes | Pizza | Desserts | Cookies | Buns & Rolls | Bars | Breakfast Products

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!