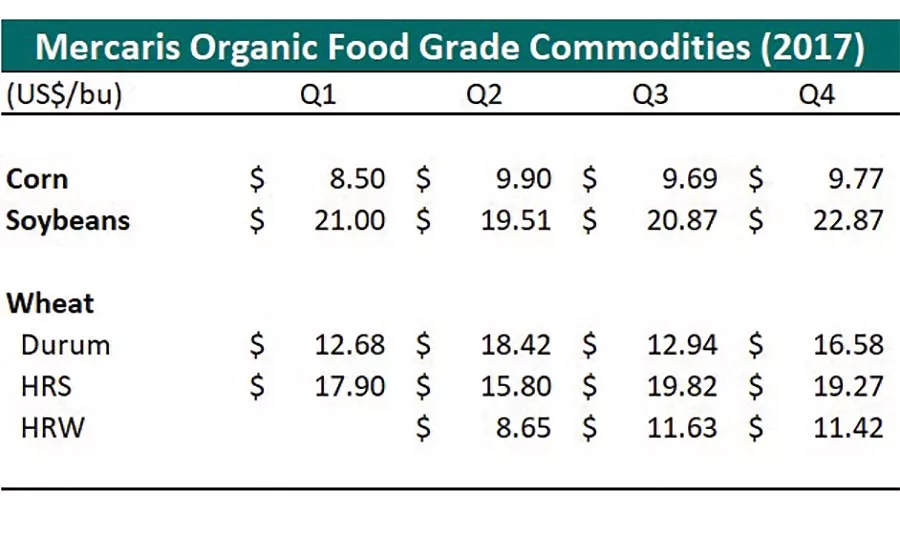

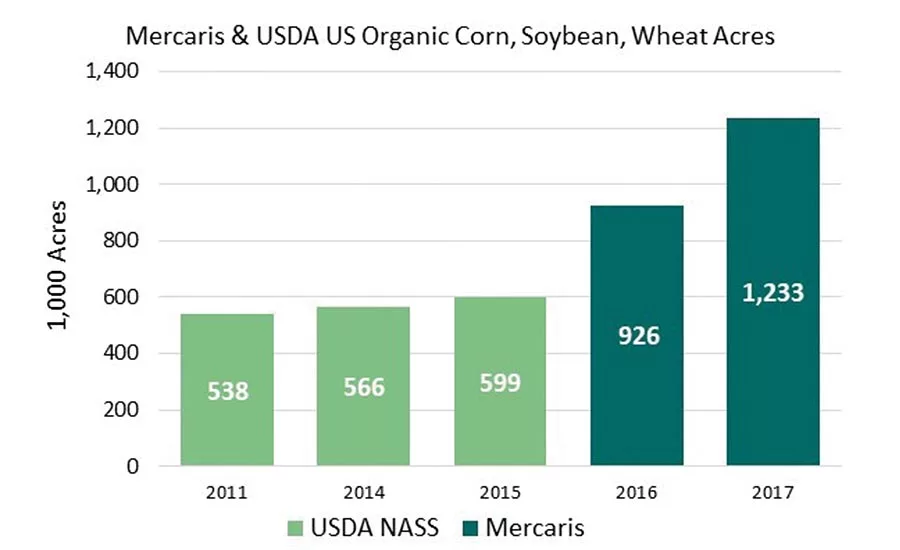

Organic commodity grain outlook

Ryan Koory, senior economist, Mercaris, Silver Spring, MD, provides insight into the current organic commodity grain outlook, including market pricing and acreage dedicated to organic grain cultivation. This is the first installment of a new, regular content perspective on the business of snack and bakery commodities.

Food use remains the minority share of U.S. organic grain and oilseed demand. But as a market driver, its importance cannot be understated. From a product-side perspective, consumers demand organic cereal and oilseed crops as either animal feed in the form of meat, or as packaged food goods like boxes of cereal, crackers, bread, etc. Due to the sizable presence of meat protein in U.S. diets, organic crop use for animal feed provides the lion’s share of demand, similar to what you see in the corn and soybeans in the conventional sector. However, unlike the conventional sector, packaged organic food goods have a lot of space to increase their market share, and there is room to provide price premiums and incentives for farmers to expand acreage.

Also, the food-grade organic market has been a bit more insulated from import competition, relative to feed markets. This is due in part to the smaller scale of the food-grade organic market relative to feed-grade. This means that an organic food-grade corn or soybean producer does have one less market to compete with when marketing their grain.

While weather and the U.S. macroeconomic climate remain uncertain variables, we know that the U.S. is expected to maintain positive economic steam through at least 2018. Also, with the exception of the extreme cold snap at the start of January, and dryness in the northern plains and southern Canada, U.S. weather isn’t shaping up to be an issue. For this 2017–18 crop year, we estimate U.S. organic corn production reached 43.6 million bushels (bu), up 39 percent from 2016–17. Soybean production is estimated at 7.1 million bu, up 38 percent from 2016–17. Wheat is also up 14 percent from 2016–17 with acreage growing more slowly, and an expectation of reduced yields following lower yields in the conventional sector. But, despite wheat’s less-stellar growth, it looks safe to say that the market will have a lot more grain to market over 2018.

Whether or not the boost in production will be enough to satisfy growth in domestic demand is a real question for consideration as 2018 starts. As mentioned above, feed demand is the largest factor when considering U.S. organic demand. Based on organic animal inventory data from USDA-NASS, we expect 2017–18 organic animal feed demand growth to outpace domestic feed demand growth. Also, organic feed imports received a black eye in September 2017 following an article in The Washington Post that highlighted fraudulent activity among organic grain importers. We also saw imports slow over the last quarter of last year. Whether this is due to the sizeable 2017–18 crop harvest or domestic feed purchases turning away from imports is hard to say at the moment. But, we can say that animal feed demand still appears to be outpacing production growth, and without imports, this discrepancy is likely to add bullish pressure and competition for contracts to the U.S. organic sector.

So, as we start 2018, U.S. organic crop production looks to continue growth at a near-astonishing rate, with key crops like wheat, corn and soybeans pulling off double-digit year-over-year growth. However, this very large crop may not be enough to provide bearish pressure for prices for long, as organic livestock production growth is remaining ahead of domestic feed supplies. Also, with 2018 expected to provide another year of macroeconomic growth for the U.S., we are likely to see U.S. packaged food consumers also increase purchases of organic products. And one market wildcard: U.S. organic livestock producers’ dependency on imports may be tested in a major way this year, which would be likely to result in significant bullish market pressure.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!