State of the Industry 2018: Crackers explore new textures and formulations

Manufacturers seek to jumpstart the cracker category with new flavors and ingredients

Crackers remain one of the most-important segments in baked snacks. But growth has stagnated in recent years. To drive sales, manufacturers are doing exciting things with flavors and other ingredients to meet culinary- and health-driven consumer demands.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Market data

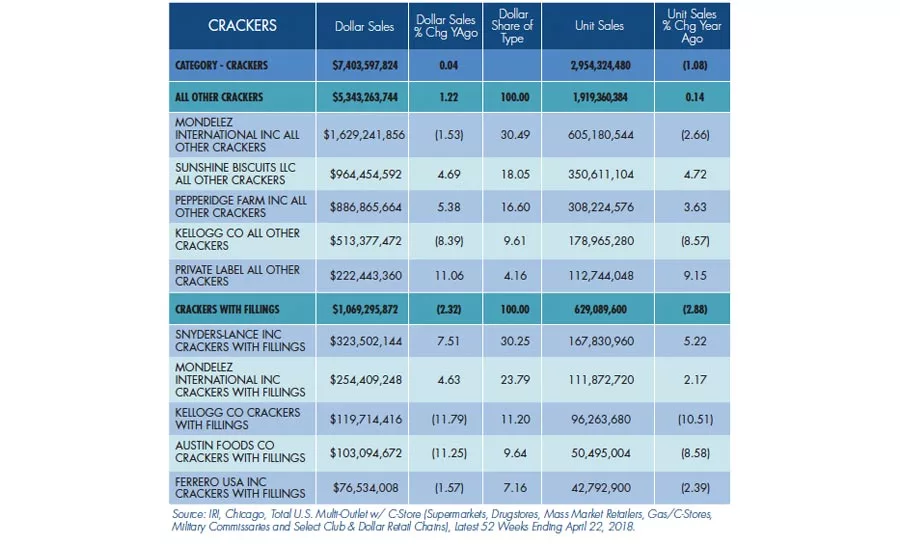

For the 52 weeks ending April 22, 2018, per IRI, Chicago, sales of crackers were relatively stable, with dollar sales growth of only 0.04 percent. But the category remains significant, responsible for $7.4 billion in dollar sales for the year.

The all other crackers segment saw the best level of growth, up 1.22 percent to $5.3 billion. Kellogg Co.’s Cheez-It brand continues its domination, up 3.35 percent to $790.2 million. Cheez-It saw strength from its Duoz line—which combines two Cheez-It flavors and/or formats of snacks—which grew 60.22 percent to $68.5 million. Campbell Soup Co./Pepperidge Farm brand Goldfish crackers likewise saw growth, up 3.58 percent to $572.8 million. Its Flavor Blasted Goldfish line grew 7.71 percent to $158.3 million, while Goldfish Colors grew 5.69 percent to $108.1 million. Classic Mondelez International brand Ritz also saw a strong year, up 8.31 percent to $540.3 million. Private label notably broke into the top 5 performers, up 11.06 percent to $222.4 million.

Crackers with fillings dropped 2.32 percent to $1.1 billion. Snyder’s-Lance, now part of Campbell Soup Co., had a strong year, up 7.51 percent to $323.5 million. The Lance ToastChee brand was up 8.52 percent to $111.4 million, while the Lance Toasty line grew 22.91 percent to $67.3 million. The main Lance sandwich crackers line grew 66.70 percent to $38.7 million. The segment-leading Mondelez brand Nabisco Ritz crackers with fillings line saw a particularly strong year, up 22.71 percent to $151.1 million.

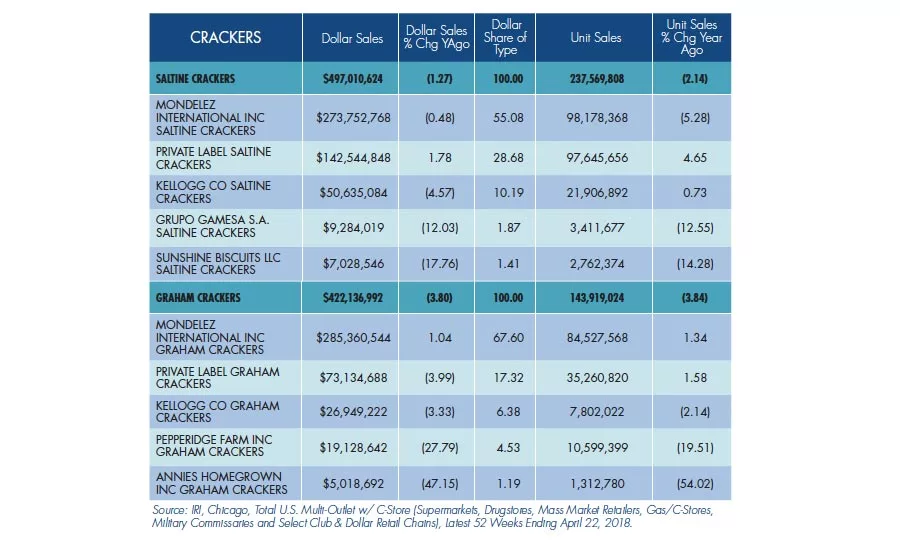

Saltine crackers dropped 1.27 percent to $497.0 million; within the top five, only private label saw a positive year, up 1.78 percent to $142.5 million.

Graham crackers dropped 3.80 percent to $422.1 million. Mondelez and its Nabisco Honey Maid line dominate the segment. The company overall grew 1.04 percent to $285.4 million, while Honey Maid grew 4.11 percent to $242.1 million, per IRI. And while Kellogg Co. overall dropped 3.33 percent to $27.0 million, its Scooby Doo line grew a healthy 10.23 percent to $23.6 million.

Looking back

It comes as no surprise that mainstream cracker shapes and formats remain most popular. “While we do see new cracker designs or shapes being tried by our customers each year, they are still consistently ordering die rolls for designs that have been around for decades,” says says Mike Kriegermeier, senior vice president, American Engraving Corp., Bensenville, IL.

The innovation comes from a flavor perspective. “We see them taking their branded crackers and trying different flavorings with them,” adds Kriegermeier. “This allows them to keep the same die design, while adding ‘new’ products to their portfolio.”

TH Foods Inc., Loves Park, IL, has been applying flavor trends to its crackers of late. The company’s Crunchmaster product line includes crunchy, gluten-free, light and crispy crackers that complement gourmet cheeses, dips and hummus, notes Kim Holman, marketing director. Many Crunchmaster varieties can also stand on their own without accompaniment.

Holman notes multiple key flavor trends impacting the marketplace:

- Hot and spicy. “We have seen this in chips, now look for it in crackers. Consumers like hot, and we think hot and spicy is a big trend for crackers.”

- Cheese. “The No. 1 flavor profile for snacks is cheese. Great-tasting cheese crackers will continue to be a trend.”

- Vegetables and fruits. “U.S. consumers are trying to get more vegetables and fruits in their diets. Crackers that can help consumers do this will do well.”

- Sweet. “Crackers have long focused on savory flavor profiles. Consumers, particularly millennials, are open to new flavors, with ‘sweet’ being one of them.”

More nutritional ingredients area also going into the mix. “Consumers are looking for crackers where the ingredients offer inherent nutrition,” says Holman. “An example of this is a whole-grain cracker made with turmeric and ginger. Both are super spices that offer nutrition.” Cauliflower is also trending forward. “We think it can move to crackers.”

Coconut also continues to expand its reach across several snack and bakery categories, and has potential in crackers, suggests Holman. She likewise notes that cracker brands should look at interesting grains like amaranth, sorghum and teff, which are also naturally gluten-free.

Increasingly there is a blur between what constitutes a snack versus a meal, notes Jennifer Swift, director of marketing, 34 Degrees, Denver. The company’s ultra-thin and crispy crackers are sold in deli departments of grocery stores throughout North America.

“It is exciting to see innovation at retail locations with on-the-go cheese and cracker boxes that contain fruit, olives and more, creating new consumer usage occasions,” says Swift who sees more growth and expansion into convenient cheese, cracker and charcuterie kits that don’t sacrifice the artisan experience.

Swift also has seen new flavors and formats on the market that expand usage occasions for deli crackers. For example, 34 Degrees recently expanded into a sweet line of cracker crisps that are available in vanilla, chocolate, sweet lemon and cinnamon.

Big-picture ingredient trends impacting the crackers market include gluten-free and free-from, protein, reduced sodium, and no artificial flavor and colors, says Carolyn F. Phillips, market insights manager, Ingredion Inc., Westchester, IL. For crackers, the company’s starches are used to improve dough properties, ease sheeting quality, improve breakage and create differentiated or improved textures.

Phillips says the “food for wellness” movement is strong in snacking and includes the use of ancient grains, seeds, fruits and plant-based extracts. Also, the “clean and simple” trend remains strong, with a focus on no additives, no preservatives and free-from foods—for example, gluten free and non-GMO.

“Protein interest remains strong, but with a move toward different protein sources,” Phillips adds. “The plant-based movement continues, with pulses playing a bigger role. Some emerging trends relate to water-based plants such as algae/seaweed, kelp and spirulina. Texture also is a big topic. Ingredients such as chia seeds, sesame seeds and sea salt are being used to create different textures in the cracker segment.”

Looking forward

R&D efforts into new cracker products will primarily revolve around creating new, differentiated textures and gluten-free formulations using alternative bases including pulses and ancient grains, to reduce fat and enhance protein, Phillips predicts.

Some of the biggest challenges are in the healthy or better-for-you categories, according to Kriegermeier, who says gluten-free crackers in particular present their own set of challenges in maintaining structural integrity. “Without gluten to provide strength to the cracker, many of our customers need to find unique ways to keep the cracker from falling apart, either on the formula side or with additional design changes to the product itself. We’ve found that while one shape may work for their traditional formula, additional components or changes are needed to maintain its shape when the formula is changed to gluten-free.”

Holman says the biggest challenge in the cracker category is breaking through all the noise to reach the consumer. “This is a very large category with entire aisles filled with crackers. Brands need to break through and drive awareness and trial. Having a strong point of difference is going to be critical. This is going to be even more difficult as more sales move to e-commerce.”

Swift says that strong collaboration between brands and retailers to create an in-store entertaining solution for consumers, such as a co-promotion between cheese and crackers, is needed to ultimately help drive sales growth for both the brand and the retailer.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!