Snack Market Overview: State of the Industry 2015

Perpetual change is the mantra for an age progressively inclined toward snacking. While flavor, format and better-for-you ingredients factor heavily into the updates we have seen in snacks over the past year, improved convenience also continues to enter into the mix. And while some categories benefit from an artisan, upscale touch, others are better served with a flavor-forward audacity that resonates with youthful demographics.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Even though change remains ever-present in the new product releases streaming onto the market, select categories still thrive on the classics. These cornerstone snacks continue to anchor categories, while a new level of diversified sophistication chips away at market share, making its presence known.

Looking back

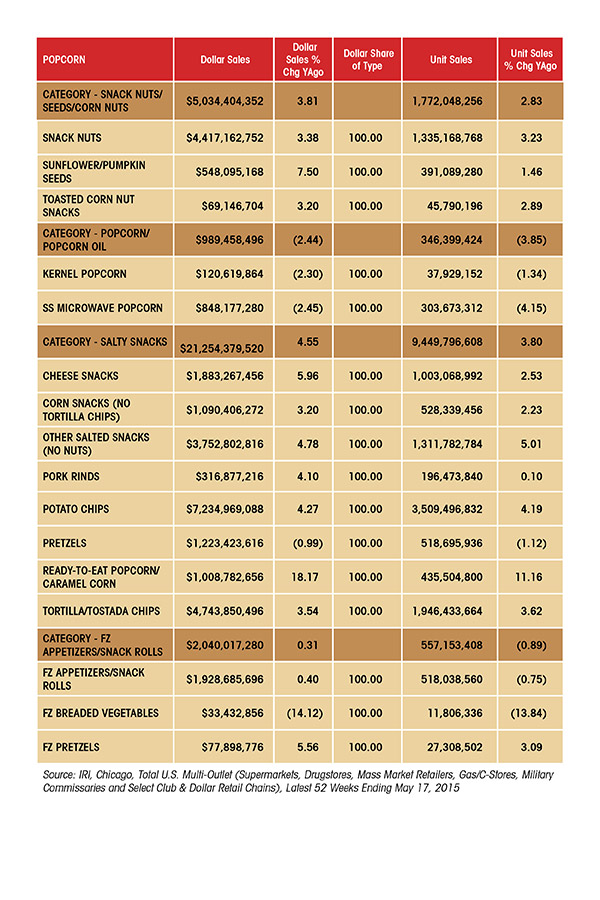

The core leaders of the snack industry continue to dominate nearly every snack category, according to data provided by IRI, Chicago. And while many of these classic brands remain largely unchanged, they’ve been joined by new products and lines that cater to the needs of different demographic segments aligned with better-for-you, flavor or just plain fun.

As Amanda Topper, food analyst, Mintel, Chicago, notes in the April 2015 “Snacking Motivations and Attitudes—U.S.” report, while nearly all Americans snack and have increased their snacking frequency over the past year, 33 percent of consumers have indicated that they are snacking on healthier foods this year compared to last year. Also, about one-third of consumers are serving healthier snacks to their children. She also notes that snacks are replacing standard daily meals—a pattern of behavior that’s likely to continue.

In the January 2015 “Salty Snacks—U.S.” report from Mintel, which covers popcorn, pretzels and puffed/extruded snacks, Topper notes that while some people remain concerned about the nutritional value of salty snacks, others have noted that they now see healthier options available, noting that 76 percent of consumers agree that the market today offers a greater amount of healthy products.

That said, 63 percent value the taste of salty snacks over their nutrition. “This attitude aligns with some consumers’ preference for indulging with salty snacks, and points to a balance between health and indulgence,” says Topper. “Taste and indulgence are main purchase drivers.”

The majority of consumers remain concerned about the nutritional value of salty snacks, with 80 percent agreeing that these items should only be eaten in moderation. More than half of consumers (56 percent) are concerned about the ingredients in these products, highlighting the need, by manufacturers, to incorporate “clean” product labels and remain transparent about ingredients, says Topper.

But what does better-for-you really mean in the eyes of today’s shoppers? These days, such definitions remain largely open to interpretation. On one hand, it can mean verifiable measures, like reduced calorie counts, added nutritional ingredients, or lower sodium and fat levels. On the other, it can mean a clean label featuring “natural” and non-GMO ingredients, portion-controlled packaging or gluten-free.

“Across category segments, product claims related to health, ingredients and allergens remain most common,” says Topper, citing findings from Mintel’s Global New Products Database (GNPD). “Natural product claims are also popular; this claim often is used in conjunction with no additives or preservatives claims. More than one in five adults who buy salty snacks (22 percent) look for products with no artificial ingredients, while 56 percent agree they are concerned about some of the ingredients in these products.”

Topper notes that the GMO-free claim has grown more than all other product claims, up 807 percent from 2009–14, per Mintel GNPD. “The claim has become increasingly visible, especially on popcorn packaging, noting the kernels were from non-GMO corn,” she says.

However, just because a claim is used more than any other doesn’t mean that it’s most important to shoppers. “Despite strong growth in use of the product claim, non-GMO ingredients are not the most-important product characteristic shoppers look for when purchasing salty snacks,” says Topper. “This may be due to confusion about GMO labeling and the definition of this claim.”

Shoppers today also tend to consider gluten-free and allergen-free/free-from foods as part of the larger better-for-you picture. “Low/no/reduced allergen and gluten-free claims grew 214 percent and 240 percent, respectively, from 2009–14, according to Mintel GNPD,” says Topper. In 2014, gluten-free hit a value of $8.8 billion.

“While many products such as popcorn and cheese puffs are naturally gluten-free, several reformulated gluten-free varieties of pretzels, from both mainstream and gluten-free-specific brands, have entered the market over the last several years,” she says. “These products have also increased their variety of flavors and formats to keep up with traditional offerings. Other allergen-free claims are mostly related to a lack of nuts or dairy.”

Gluten-free pretzel products new to the market include:

- Snyder’s-Lance Snyder’s of Hanover Gluten-Free Hot Buffalo Wing Pretzel Sticks

- Snyder’s-Lance Snack Factory Pretzel Crisps Gluten Free Vanilla Yogurt ?Flavored Crunch Minis

- Boulder Brands Glutino Gluten-Free Salted Caramel Covered Pretzels

The tortilla chips segment of salty snacks has also seen recent better-for-you developments. “A range of healthy product claims increased for tortilla chip products in 2014, including low/no/reduced trans fat, allergens and cholesterol, as well as no additives/preservatives,” says Topper. “In the past, tortilla chips enjoyed a perception that they are healthier than some other snack foods, but as snacking increases, consumers scrutinize these products more closely. Many tortilla chip brands have answered this demand with a wider range of healthy claims. Tortilla chip brands also blend corn with other vegetables to increase the flavor and health quotient.”

Recent tortilla chip launches that lean in a better-for-you direction include:

- Snyder’s-Lance Eatsmart Whole Grain Tortilla Chips, made with whole-grain corn, sesame seeds, chia seeds and quinoa flakes

- Frito-Lay Tostitos Artisan Recipes Roasted Garlic & Black Bean Tortilla Chips, made with whole-grain corn, black beans, whole wheat, whole triticale, whole oats, whole rye, whole barley, whole millet, whole buckwheat and whole brown rice

- RW Garcia Sweet Potato Dippers, made with white corn, sweet potato, flax seeds, black sesame seeds and chia seeds

Snak King The Whole Earth Really Seedy Multigrain Tortilla Chips, made with whole-grain brown rice, masa flour, flax seeds, sesame seeds, oat fiber and chia seeds

Portion control remains another viable route to better-for-you. “Smaller snack sizes and better-for-you products are a large part of product innovation within the salty snacks category,” says Topper. While this can come in the form of portion-controlled packaging, it also sometimes means smaller snacks. One example, she notes, is the rise of “pretzel thins” or otherwise “skinny” products, often in a variety of sweet and savory flavors.

Other products, such as popcorn, have tended to emphasize how “light” they are, says Topper, both in terms of seasoning or artificial ingredients. “Many products feature claims such as ‘lightly salted’ or ‘slightly sweet,’” she says.

Puffed and extruded snacks increasingly go a better-for-you route via use of alternate bases, such as vegetables, pulses and sprouted grains. As was the case elsewhere in food over the last several years, quinoa has started to appear in sweet and savory snacks, notes Topper. “Other bases, including rice, lentils and peas, are also increasingly present in a variety of salty snacks,” she says. According to Mintel’s GNPD, pea protein is most used in snacks, accounting for 15 percent of launches.

Recently released puffed and extruded snacks made with diverse bases include:

- Angie’s BOOMCHICKAPUFF, made with corn, quinoa and sorghum

- Cornfields Inc.’s Hi I’m Skinny Quinoa Sticks, made with quinoa and chia seeds

- Boulder Canyon Organic Veggie Sticks, made with organic vegetables like carrots, kale, red bell peppers, sweet potatoes, spinach, broccoli and more

- Beanitos Puffs, made with navy beans

- Simply 7 Snacks Quinoa Chips, made with quinoa

Price point is typically a big part of the reason why more shoppers are buying private label snacks. “More than half of adults who buy salty snacks (54 percent) agree store brand salty snacks are just as good—in quality, taste, etc.—as name brands,” says Topper. “The quality and variety of these products have improved, and several private label products within the category are nearly identical in format and flavor compared to their branded counterparts.” She notes that within the pretzel segment, private label sales grew 14 percent from 2013–14, more than any other manufacturer.

Private label can also mean national-brand-better innovation, with retailers building their own brand presence. The chips segment of salty snacks continues to foster strong private label innovation, including products like:

- Whole Foods 365 Everyday Value

- Tamarind Baked Naan Chips

- Trader Joe’s Potato Chips with South African Style Seasoning

- Target Archer Farms Grilled Cheese Potato Chips

- Walgreens Delish Crunchy Cinnamon Apple Chips

Looking forward

Capturing more shopper snack dollars often depends on offering the right mix of products. In “Snacking Motivations and Attitudes—U.S.,” Topper notes that 60 percent of snackers wish there were more healthy snack options, including 70 percent of households with children.

In “Salty Snacks—U.S.,” Topper notes that this $5.6 billion category grew 15 percent from 2009–14 and is expected to grow an additional 21 percent from 2014–19, benefiting from the increase in Americans snacking more often. “As other food and beverage categories enter the snacking space,” she says, “manufacturers must promote the unique benefits of their products, including their variety of flavors and formats, convenience, taste and affordability.”

As part of Mintel’s January 2015 “Chips, Salsa & Dips—U.S.” report, Topper notes that this segment was worth an estimated $14.8 billion in 2014, with projections that it will reach $17.4 billion by 2019. “Sales are primarily driven by growing snacking behavior in the U.S., as well as expanding consumer palates that demand the frequent introduction of new styles and flavors,” she says, pointing toward new chips that combine flavor with healthier ingredients, such as hybrid chips that blend corn, potato and other vegetables, to fuel growth.

The combined need for products to balance flavor and better-for-you ingredients is a common theme across most snack segments. Such is the case in frozen snacks and appetizers. The April 2015 Mintel report, “Frozen Snacks—U.S.” echoes the relatively flat performance noted by IRI’s data. “Households with children remain the $4.5 billion category’s key audience,” says Topper, “but growing the category will require healthier reformulations, novel formats and flavor innovation.”

And while snacks have certainly grown more convenient through the years, manufacturers apparently haven’t yet taken this product aspect as far as consumers would prefer. In “Snacking Motivations and Attitudes—U.S.,” Topper notes that one-third of snackers state that there aren’t enough conveniently packaged snacks, such as individual portions or resealable packages, on the market. She notes that this sentiment particularly resonates in households with children, where 42 percent believe the industry lacks a sufficient number of convenient snacks. The trick is to bring these packaging innovations to market without an undue influence on purchase price, which could potentially slow growth.

Much of this is a question of offering just the right product mix to hit all key target demographics. “With more-frequent snacking occasions and a shift away from three square meals per day, the need for a variety of snacks will increase,” says Topper. “Snacking has become nearly universal—94 percent of U.S. adults snack at least once daily—which is good news for snack manufacturers. Health will continue to play a role in the types of snacks consumers are interested in. However, it’s important to recognize the impact of flavor and satisfying a craving on snacking occasions, which occasionally trump health.”

The top reasons consumers buy salty snacks is as a treat (60 percent) or to satisfy a craving (58 percent), notes Topper, highlighting the important role flavor plays in the category. “While better-for-you options are important to consumers, they should not come at the expense of a great tasting product,” she says. “Consumers should not feel like they are sacrificing taste for health.”

A weighty question today centers on how long the gluten-free boom will last—a phenomenon that has impacted every corner of snacks. “The category continues to thrive, as awareness of gluten-free foods increases,” says Topper. “Increasing diagnoses of celiac disease and other gluten sensitivity, as well as the popularity of eating a gluten-free diet for other perceived health benefits, including for weight loss, more energy or athletic performance, are key market drivers.” She notes that 82 percent of consumers who report eating gluten-free foods have not been medically diagnosed with celiac disease, and 44 percent go gluten-free for reasons other than gluten intolerance or sensitivity.

“Gluten-free products appeal to a wide audience; 41 percent of U.S. adults agree they are beneficial for everyone, not only those with a gluten allergy, intolerance or sensitivity,” says Topper. “In response, food manufacturers offering either gluten-free alternatives or existing products with a gluten-free label have increased dramatically over the last several years. As greater demand for gluten-free foods increases, whatever the reason may be, new players continue to enter the market.”

Topper suggests that gluten-free will continue to grow—albeit at a slightly smaller rate. “Looking ahead, Mintel predicts the gluten-free food category will grow an additional 62 percent from 2014–17, to reach sales of $14.2 billion in 2017,” she says. “However, year-over-year growth is likely to become more modest compared to previous year-over-year increases.”

Growth in specialized niches within snacks, such as gluten-free and better-for-you, will progressively moderate—but each collective trend points toward multiple sound formulation strategies for the future. While select classic snacks will continue to soldier forward largely unchanged, manufacturers will provide support via other lines, products and brand extensions that clearly highlight flavor diversifications and nutritional improvements—with the more astute products of the bunch perhaps eventually destined to achieve classic status for a new generation of consumers.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!