Snack Market Overview: State of the Industry 2016

Every leading segment of snack products has grown or evolved to accommodate shifting consumer preferences for their favorite snacks.

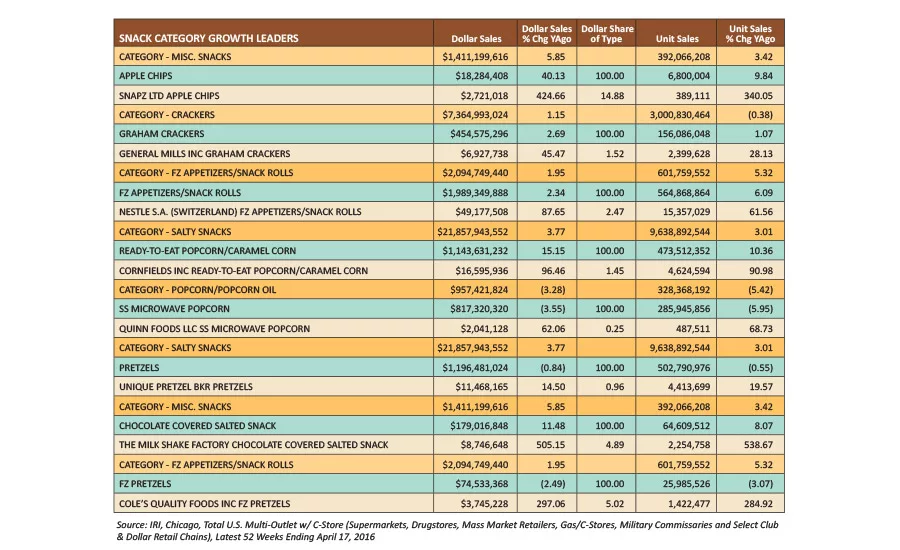

SNACK CATEGORY GROWTH LEADERS

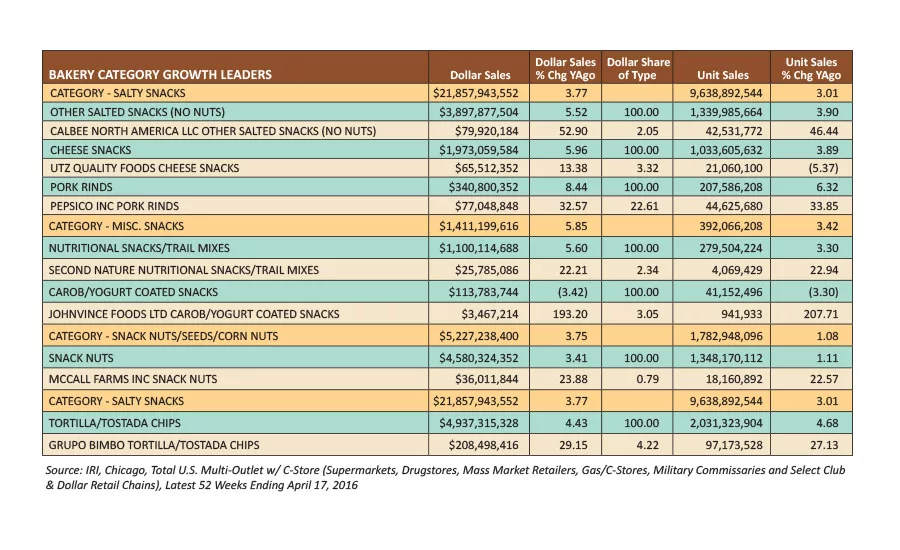

BAKERY CATEGORY GROWTH LEADERS

Snacks are ingrained within U.S. consciousness. We’re a snacking culture. It’s built into our DNA.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Peanuts—perhaps America’s first snack food—traveled the seas from their South American origins to Africa, and then finally to the young British colonies. Not long after, pretzels followed German and Dutch immigrants to the newly formed United States. Popcorn, a popular American street food in the 1800s, is synonymous with special events like fairs, festivals and—of course—trips to the movie theater. And while varied versions of toothsome hardtack have existed for hundreds of years, it took American ingenuity to bring the lightly leavened—and dramatically more appealing—saltine cracker to life in the 1870s.

Nearly every major snack—from potato and corn chips to cheese snacks—has a tale to tell, and all found fertile soil to flourish in the U.S.

And now snacks aren’t simply relegated to special occasions and between meals—snacks are a way of life. We have become a nation of snackers. According to the April 2015 report, “Snacking Motivations and Attitudes—U.S.,” from Mintel, Chicago, 94 percent of Americans snack every day—and half of all U.S. adults snack two to three times per day.

But meeting the diverse snacking needs of today’s U.S. population requires sound tactical consideration regarding whether tradition—or a subtle to pronounced better-for-you spin—should prevail in any given scenario.

Looking back

Multiple categories across snacks were home to breakout brands that saw notable sales gains over the 52 weeks ending April 17, 2016, per IRI, Chicago.

The 40.13 percent growth in dollar sales for the apple chips segment is groundbreaking. That level of growth should turn heads from across the snack industry—and clearly anyone working within chips. While this growth is undoubtedly drawing purchases from consumers typically not prone to buying traditional potato chips, some share shift is expected.

Five apple chips companies within the top 10 saw dollar sales growth over 100 percent for the past year. Even in traditional chip segments, we’re starting to see a wider diversity of chip bases factoring into product development, making use of other root vegetables beyond potatoes like beets, parsnips, sweet potatoes and yucca. Vegetable diversity is an appealing selling point—as long as flavor stands up to scrutiny. This trend toward chip diversification will continue over the next few years as we see how much growth these segments can sustain.

Frozen snacks and appetizers have faced their fair share of challenges over the past few years, but the segment saw a bit of promising growth over the past year. Nestlé was the standout company in the segment, with dollar sales up by 87.65 percent, largely thanks to the performance of its Hot Pocket Bites line. The brand has built strong resonance with millennial shoppers and is seeking to continue this relationship with its new addition of Hot Pockets Food Truck Bites, which elevate the culinary sophistication of the line and add some touches of ethnic diversity.

Another big move over the past year came in the microwave popcorn segment. While ready-to-eat popcorn has been trending forward for a few years now—a pattern that continued over the past 52 weeks—microwave has seen steady drops. That pattern continued over the past year, with dollar sales falling by 3.55 percent. But one company managed a particularly strong showing. Quinn Foods saw sales of its clean-label microwave popcorn rise by 62.06 percent. A key piece of this puzzle is the strong level of innovation that went into designing a new bag for the products.

Unique Pretzel Bakery—the 2016 Snack Food & Wholesale Bakery “Snack Producer of the Year”—continues to find a strong audience for its Unique Splits products, which grew by 14.50 percent in dollar sales, well outperforming the category average. National expansion of the brand continues, so we expect to see growth continue. Fans of the products like the artisan nature of the product, which gives it specialty-product appeal without a jump in price point. We also expect to see notable sales gains for its sprouted grain pretzels, available in both Shells and Splits, as word of their nutritional merits spreads.

Private label maintains a solid presence across all snack categories. According to the 2016 Private Label Manufacturers Association (PLMA) “Private Label Yearbook,” private label snacks accounted for $1.1 billion in sales last year. PLMA tracks nuts separately, and that segment of snacks adds another $859.7 million in revenue, accounting for 33.4 percent of dollar share for the category.

Private label leads the nutritional snacks/trail mixes segment, as well as the snack nuts segment. Per IRI, over the past year, private label saw $536.4 million in revenue in nutritional snacks/trail mixes, and $1.3 billion in snack nuts.

Unlike in bakery, where private label dominates multiple categories, in snacks we still see strong national brand performance among category leaders.

However, avenues for developing new private label business exist in snacks. Private label does not have a presence among the top companies in the fast-growing apple chips category, presenting an opportunity for store brand penetration. And considering the appeal mixed bags of chips have seen, a national-brand-better retail brand looking to capture market share in the segment might consider a product that combines various fruit chips, such as apple and pear, with a clear, clean label and strong better-for-you product positioning.

Looking forward

Better-for-you dynamics continue to factor into new product development across snacks. While traditional snack products still perform quite well—and will continue to do so—incremental growth has come from new better-for-you products that have built platforms on baked vs. fried and use of diverse substrates, like vegetable and lentil powders—an approach that has worked well in segments like extruded snacks.

Including these vegetable-based ingredients in product formulations at levels that permit verifiable claims related to ingredient and nutrient levels will help build appeal. For instance, Calbee North America’s Harvest Snaps brand includes a highly visible “More Than 70% Whole Green Peas” claim on the back of the package, while the front of the pack includes verbiage like “Baked,” “50% Less Fat,” “Good Source of Fiber” and “Low Sodium.” These messages resonate with female, health-oriented shoppers who frequent the specialty grocery channel. It’s a product platform that moms feel comfortable with offering to their children.

The extruded snacks segment can continue its positive growth trajectory through use of diverse, sprouted and/or ancient grains to reach shopper demographics not sensitive to gluten-free claims, but who have unmet needs for nutrition-forward snack alternatives. Such products should include messaging that clearly illustrates the nutritional merits of whole-grain snacks.

FDA’s updated structure for the Nutrition Facts panel will undoubtedly catalyze new thinking during the research and development of snack products. The text for “Calories” is now dramatically larger, so efforts to reduce calorie counts per serving will see new life. Also, the addition of “Added Sugars” information will also factor into product design, opening the door to innovation with ingredients that inherently bring sweetness to formulations to reduce the use levels of caloric sweeteners.

On the flip side, indulgence still finds a willing audience in snacks today, as we saw with the growth of the chocolate covered salted snack segment. The combination of salty and sweet still sells, and the scalable portion sizes of snackable, dessert-like products works well for consumers looking for little indulgences to brighten snack times.

As America continues to develop its long-term relationship with snacking, a reasonable approach toward balancing classic, traditional and, yes, even indulgent products with next-generation better-for-you, clean-label snacks will emerge. We want the best of both worlds, and don’t want to compromise on either.

Overview | Chips | Puffed/Extruded Snacks | Popcorn | Snack Mixes & Nuts | Tortilla Chips | Pretzels | Frozen Snacks | Crackers

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!